Ethereum

Ethereum Hyperliquid

Hyperliquid Solana

Solana Arbitrum

Arbitrum BNB Smart Chain

BNB Smart Chain Base

Base Polygon

Polygon TRON

TRON Sui

Sui Robinhood

Robinhood

Top 6 RWA tokenization platforms in 2026

Real-world asset tokenization crossed $30B in distributed on-chain value in July 2026 (RWA.xyz). But that value isn’t evenly distributed across the 183 platforms tracked. Six pure tokenization platforms account for over half of it — and each takes a fundamentally different approach to compliance, chain coverage, and target investor base.

This guide ranks the six leading pure-play RWA tokenization platforms in 2026: their TVL, chain support, compliance models, best-fit use cases, and honest limitations. If you’re evaluating platforms to issue on, integrate with, or invest through, this is the shortlist that matters.

For the broader context of what a tokenization platform is and how the layers of the RWA stack fit together, see our pillar guide: What is a tokenization platform? RWA leaders, standards & compliance in 2026.

Positioning note: Chainstack is an RPC infrastructure provider. We sit below tokenization platforms in the stack, not alongside them. This ranking is written from that vantage — we care about which platforms actually deliver production-grade on-chain infrastructure that our customers depend on.

How we ranked (and what we excluded)

The ranking uses RWA.xyz distributed value (July 2026 snapshot) as the primary sort key, filtered to pure tokenization platforms — companies whose primary business is tokenization middleware, not stablecoin issuance or single-product asset management.

What we excluded from top 6 (and why):

- Stablecoin issuers (Circle $3.11B, Tether $2.47B, Paxos $1.85B) — their treasury tokenization is a side-product of stablecoin operations. Reader searching “top tokenization platforms” wants general-purpose middleware, not USDC/USDT issuers.

- Single-product asset managers (Franklin Templeton Benji $2.47B, WisdomTree $754M) — issue their own tokenized fund on their own infrastructure. Not a platform others can build on.

- Backed Finance ($720M via xStocks) — moved to Honorable Mentions. Excellent equity-tokenization specialist, but xStocks is a consumer brand more than a platform for third-party issuers.

Ranking criteria (in priority order):

- RWA.xyz distributed value (primary sort)

- Chain coverage and multi-chain architecture

- Compliance model maturity and institutional integrations

- Developer experience (integration surface, documentation, SDK availability)

- Regulatory clarity and jurisdictional coverage

Comparison table

| # | Platform | TVL | Best-fit | Chains | Compliance model |

|---|---|---|---|---|---|

| 1 | Securitize | $4.39B | US institutional issuance, funds | Ethereum, Solana, Arbitrum, Polygon, Aptos, Avalanche, Optimism | DS Protocol (preTransferCheck) |

| 2 | Ondo Finance | $3.62B | Retail + qualified treasuries, tokenized stocks | Ethereum, Solana, Mantle, Sui, Aptos, XRP, BNB | Blocklist (USDY) + KYC registry (OUSG) |

| 3 | Spiko | $2.05B | EU corporate treasury (UCITS MMF) | Ethereum, Stellar, Base, Polygon, Arbitrum, Starknet, Etherlink | UCITS regulatory + KYC allowlist |

| 4 | Centrifuge | $1.64B | Private credit, DeFi-native funds | Ethereum, Base, Arbitrum, Avalanche, Plume, BNB, Optimism | ERC-1404 + ITransferHook (V3 hub-and-spoke) |

| 5 | Maple Finance | $1.42B | Institutional credit, permissionless yield | Ethereum, Base, Solana, Arbitrum, Plasma | Bitmap permission manager + open ERC-4626 |

| 6 | STOKR | $1.32B | Bitcoin-native structured notes, hashrate | Liquid Network (Bitcoin sidechain) | MiFID II eligible investor + KYC |

Data source: RWA.xyz, July 2026 snapshot. TVL figures move; verify before making investment or integration decisions.

1. Securitize — the institutional standard

TVL: $4.39B · Founded: 2017 · HQ: Miami / NYC · CEO: Carlos Domingo

Securitize is the category leader by a wide margin. It powers BUIDL (BlackRock’s tokenized money market fund — the single largest RWA on-chain) and ACRED (Apollo Diversified Credit Fund), and holds ~20% of the total tokenization platform market by AUM.

What makes Securitize different: the fully regulated stack. Securitize operates as an SEC-registered transfer agent, broker-dealer (Securitize Markets), ATS operator, investment adviser, and fund administrator — simultaneously. Most competitors handle one or two of these; Securitize does all five under one roof.

Compliance runs through the proprietary DS Protocol — the most mature on-chain compliance system in production. Every transfer calls preTransferCheck(), which simulates the transfer gaslessly against the on-chain Compliance Service and returns validity plus a reason code before execution. It enforces OFAC sanctions, jurisdictional caps, holder limits, and forced-transfer capabilities for regulator interventions.

Best-fit use case: US institutional issuers requiring the full regulated stack. If you’re a BlackRock, Apollo, KKR, or Hamilton Lane bringing a fund on-chain and need transfer-agent, broker-dealer, and ATS services from the same counterparty, Securitize is the default choice. Also strong for cross-border funds requiring Delaware LLC or BVI wrappers with jurisdictional enforcement at the token contract level.

Chains supported: Ethereum, Arbitrum, Polygon, Aptos, Avalanche, Optimism, Solana, Ink. BUIDL alone lives on 7+ chains simultaneously, with LayerZero-based cross-chain messaging.

Recent trajectory: Securitize went public via SPAC merger with Cantor Equity Partners II at a $1.25B valuation, listing on NYSE as SECZ on July 2, 2026 with ~$400M gross proceeds plus a $225M PIPE. Q1 2026 revenue was $19.5M (+39% YoY).

Why not Securitize: Overkill for permissionless DeFi-native yield products. If your use case is a public-facing ERC-4626 vault targeting retail crypto users, the DS Protocol’s whitelist model is too heavy. Also, integration cost is high — the DS Protocol is proprietary and requires bespoke work to integrate downstream (indexers, dashboards, wallets).

2. Ondo Finance — the largest treasury issuer

TVL: $3.62B · CEO: Ian De Bode · 440 RWAs

Ondo Finance leads the tokenized-treasury vertical and has expanded aggressively into tokenized equities in 2026. Where Securitize serves institutional issuers, Ondo serves the direct investor with retail-friendly access to US treasuries and — as of 2026 — tokenized US public equities.

Product portfolio:

- USDY (~$740M) — non-US retail secured note backed by Treasuries + bank deposits; ~4.65% APY. Blocklist compliance.

- OUSG ($407–479M) — US qualified purchasers only under Rule 3(c)(7); backed primarily by BUIDL. KYC registry compliance.

- Ondo Global Markets (~$1B) — 100+ tokenized US stocks and ETFs. Crossed $1B in May 2026; >70% market share of tokenized-stock volume.

- Ondo Chain — institutional L1 with permissioned validators staking RWAs; mainnet targeted mid-2026.

Compliance model split by product: USDY uses a blocklist (permissionless-friendly, deny-list based). OUSG uses a KYC registry (allowlist only for whitelisted addresses). Same issuer, two products, two compliance models targeting different investor bases. It’s a clean example of how compliance isn’t one thing.

Best-fit use case: Retail non-US access to US Treasury yield (USDY), qualified US access to institutional treasuries (OUSG), or on-chain exposure to specific US stocks (Ondo Global Markets). Also strong for teams building DeFi integrations — USDY especially is designed for composability with lending protocols and DEXes.

Chains supported: Ethereum, Solana, Mantle, Sui, Aptos, XRP Ledger, BNB Chain. Bridge sits on LayerZero.

Recent trajectory: Ondo Global Markets crossed $1B TVL on May 11, 2026 and now leads tokenized US stocks with >70% market share. The SEC closed its investigation into Ondo in December 2025 without charges — regulatory tailwind.

Why not Ondo: Not a general-purpose tokenization platform in the Securitize sense. You can’t bring your own asset and have Ondo tokenize it — Ondo issues its own products. If you’re an asset manager looking for tokenization-as-a-service, look at Securitize, Centrifuge, or Spiko instead.

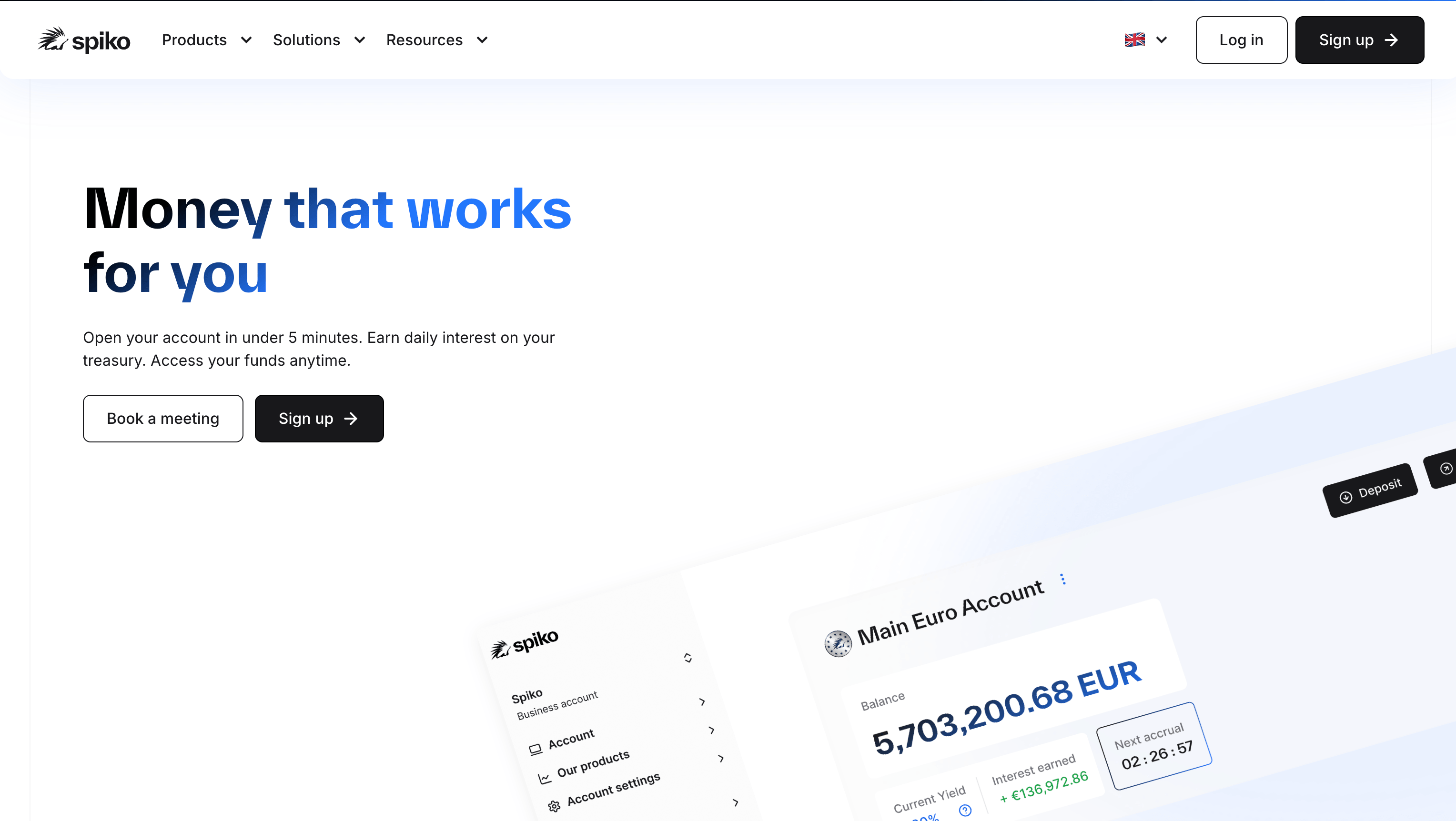

3. Spiko — Europe’s tokenized MMF leader

TVL: $2.05B · Founded: 2023 · HQ: Paris · Co-founders: Paul-Adrien Hyppolite & Antoine Michon

Spiko is the newer entrant in the top 6 and the one most Chainstack readers won’t have heard of yet. Founded in 2023 by two former French senior civil servants, Spiko is Europe’s first UCITS-approved tokenized money market fund platform — and it crossed $1B AUM by January 2026, doubled by July.

Product portfolio:

- Spiko EU T-Bills MMF (EUTBL) — Eurozone Treasury Bills, UCITS-approved, ~$1B market cap

- Spiko US T-Bills MMF (USTBL) — US Treasuries, UCITS wrapper for EU investors

- Spiko UK T-Bills MMF (UKTBL) — UK gilts

- SAFO — Spiko Amundi Overnight Swap Fund, launched March 2026 with Amundi (Europe’s largest asset manager), Chainlink NAV oracle

What makes Spiko different: regulatory positioning. Spiko products are structured as UCITS funds regulated by the AMF (France), distributable across all 27 EU member states under a single passport. Investors deal with a familiar UCITS wrapper — tokenization is an infrastructure choice, not a legal restructuring. For EU corporate treasuries and SMEs, this removes almost all onboarding friction.

Best-fit use case: European corporate treasury management. SMEs and fintechs looking to earn risk-free rate on idle Euro or USD cash — with UCITS regulatory clarity, MiFID II compatibility, and 24/7 tokenized redemption to stablecoins. Spiko’s B2B distribution via API integrations with fintech partners has driven most of its growth.

Chains supported: Ethereum, Stellar (primary), plus Base, Polygon, Arbitrum, Starknet, and Etherlink for EUTBL.

Recent trajectory: Series A of $22M led by Index Ventures in July 2025 (Revolut’s Storonsky and Blackstone’s Assant among angels). Integrated Coinbase Payments in mid-2026 — the first EU-regulated funds to accept stablecoin subscriptions, per the Coinbase-Spiko announcement (FinanceFeeds, July 2026).

Why not Spiko: Non-EU issuers can’t easily use Spiko as a platform — the UCITS structure is EU-native. Also, product depth is treasury/MMF-focused. Private credit, equities, real estate — Spiko doesn’t touch these.

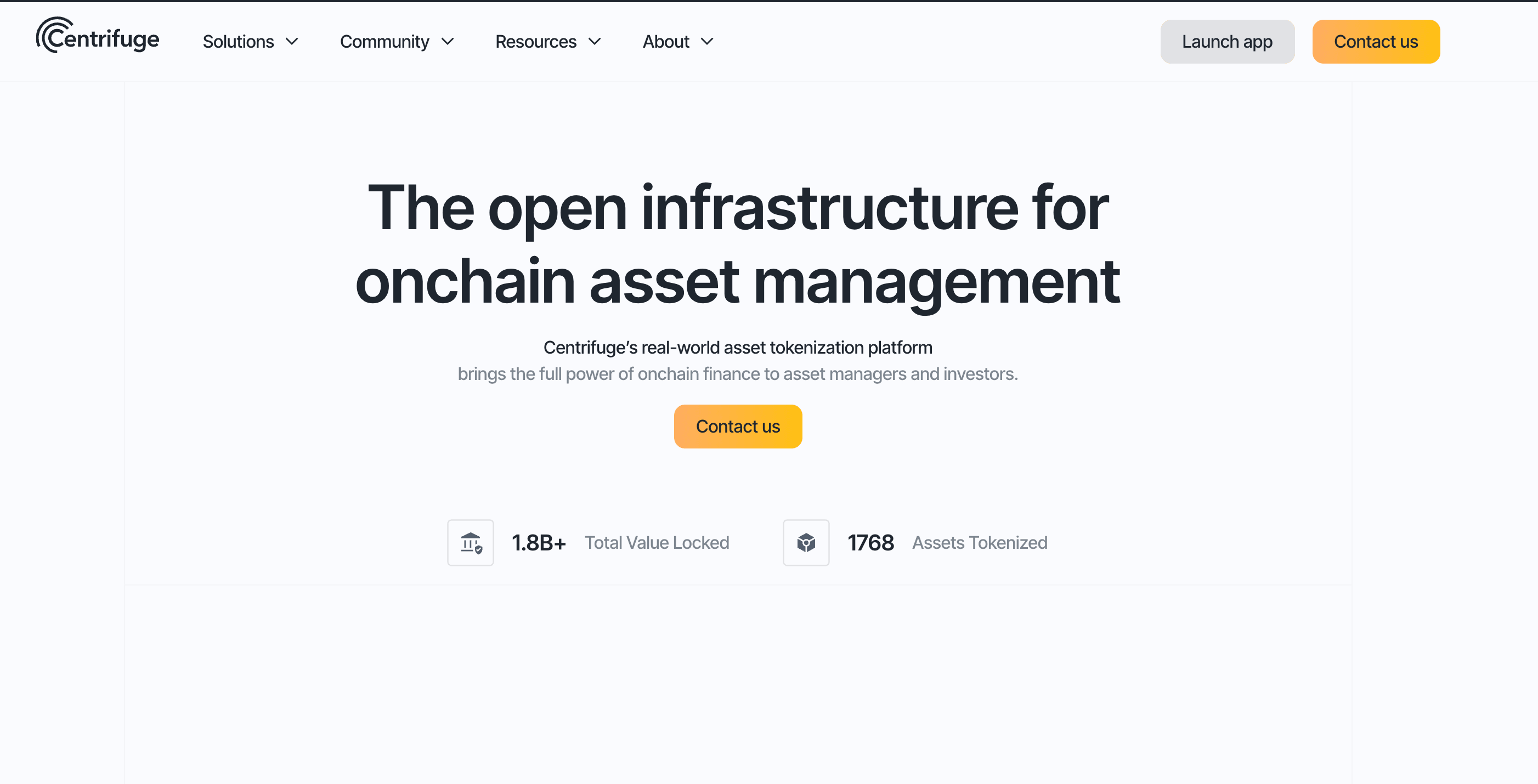

4. Centrifuge — private credit and DeFi-native

TVL: $1.64B · Founded: 2017

Centrifuge is the private-credit tokenization pioneer and the first to bring RWA collateral into DeFi (via MakerDAO in 2020). In 2026, its differentiator is V3 architecture, launched July 2025 — a full rewrite from Polkadot parachain to multichain EVM-native.

V3 hub-and-spoke architecture: each pool picks one hub chain (for accounting, NAV, pricing) and issues share tokens on multiple spoke chains via burn-and-mint. Cross-chain messaging aggregates LayerZero, Wormhole, Chainlink, and Axelar — no lock-in to a single bridge.

Product portfolio:

- JTRSY ($875.8M) — Janus Henderson Anemoy Treasury; largest on Centrifuge

- JAAA — AAA CLO fund, peaked ~$700M

- deSPXA — S&P 500 index fund on Base (Janus Henderson under S&P Dow Jones license)

- deRWA distribution engine for third-party issuers

Compliance model: Share tokens are ERC-20 with ERC-1404 restriction compatibility and ITransferHook compliance hooks. Vaults implement ERC-4626 (synchronous) and ERC-7540 (asynchronous, for slow-settling RWA). This is unusual: Centrifuge uses standard ERC interfaces rather than a proprietary protocol, which makes downstream composability much easier than DS Protocol.

Best-fit use case: Private credit funds targeting DeFi liquidity. If you want tokenized fund shares that Aave Horizon, Morpho, Pendle, or Spark can accept as collateral out of the box — Centrifuge’s ERC-4626/7540 conformance is why.

Chains supported: Ethereum, Base, Arbitrum, Avalanche, Plume, BNB Chain, Optimism, with HyperEVM and Monad in progress.

Recent trajectory: Won Spark’s $1B Tokenization Grand Prix in 2025 with a $200M JTRSY allocation. 19 security audits shipped. Composable with Sky (formerly MakerDAO), Aave Horizon, Morpho, and Pendle.

Why not Centrifuge: Not designed for retail-facing US products. If you need SEC-registered transfer agent + broker-dealer under one roof, Securitize is the answer. Centrifuge is DeFi-first, TradFi-composable — the opposite direction from Securitize’s regulated-first stack.

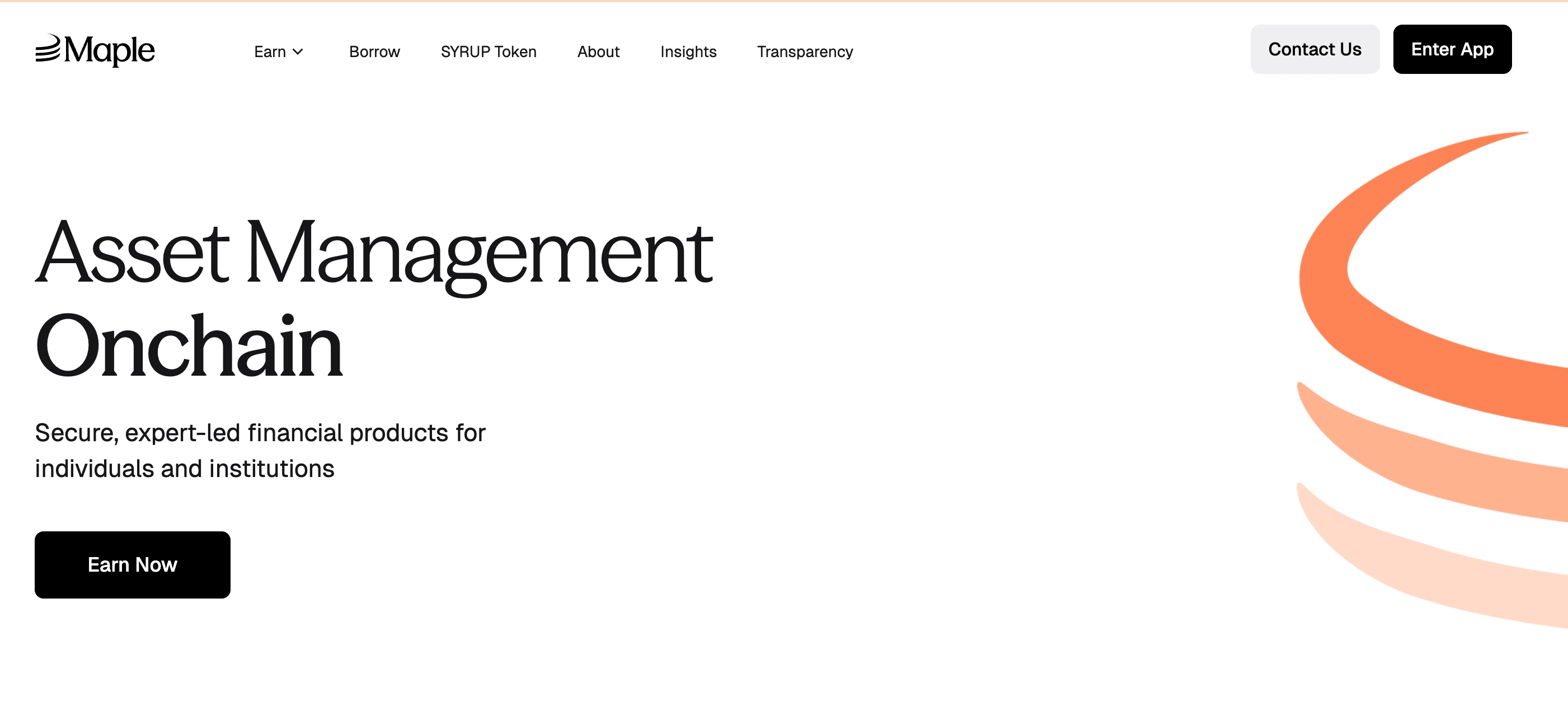

5. Maple Finance — institutional credit + syrupUSDC

TVL: $1.42B · Founded: 2019 · CEO: Sid Powell (ex-National Australia Bank)

Maple Finance started as institutional undercollateralized crypto lending, restructured after the 2022 Orthogonal default, and has posted zero losses since 2023 with all loans >150% collateralized. In 2026, its differentiator is the dual product structure: institutional pools with strict compliance, and permissionless yield tokens for the broader DeFi audience.

Product portfolio:

- Blue Chip Secured and High Yield Secured institutional pools (compliance-gated)

- Cash Management Vault — tokenized T-bills

- Maple BTC Yield — Bitcoin-denominated institutional lending

- syrupUSDC and syrupUSDT — permissionless ERC-4626 yield tokens; syrupUSDC alone sits at ~$1.29B TVL with 6–10% APY

Compliance model: Two tiers. Institutional pools use a bitmap permission manager — a gas-efficient on-chain bitmap encoding eligibility per address. syrupUSDC uses nothing — it’s an open ERC-4626 vault, no KYC gate, composable everywhere. It’s the cleanest example of “one platform, two compliance models for two investor bases” in the market.

Best-fit use case: Institutional crypto credit desks needing on-chain lending against Bitcoin, Ethereum, and Solana collateral (institutional pools). Or DeFi builders looking for a stable yield token composable with Aave, Morpho, Pendle without dealing with allowlists (syrupUSDC).

Chains supported: Ethereum, Base, Solana, Arbitrum, Plasma. Multi-chain via Chainlink CCIP CCT burn-and-mint — cleanest cross-chain implementation among the top 6.

Recent trajectory: Proof of Reserves attestation via The Network Firm, launched May 7, 2026 for syrupUSDC and syrupUSDT. Integrations with Pendle, Morpho, Aave. Kraken warehouse-lending facility. Bitwise allocation. MPL → SYRUP token migration completed 2025.

Why not Maple: Institutional lending focus is narrower than Securitize or Centrifuge. If your use case is tokenized public equities, real estate, or non-credit RWA — Maple isn’t relevant. Also, Maple is chain-selective: mostly EVM + Solana, no Aptos/Sui/Stellar exposure.

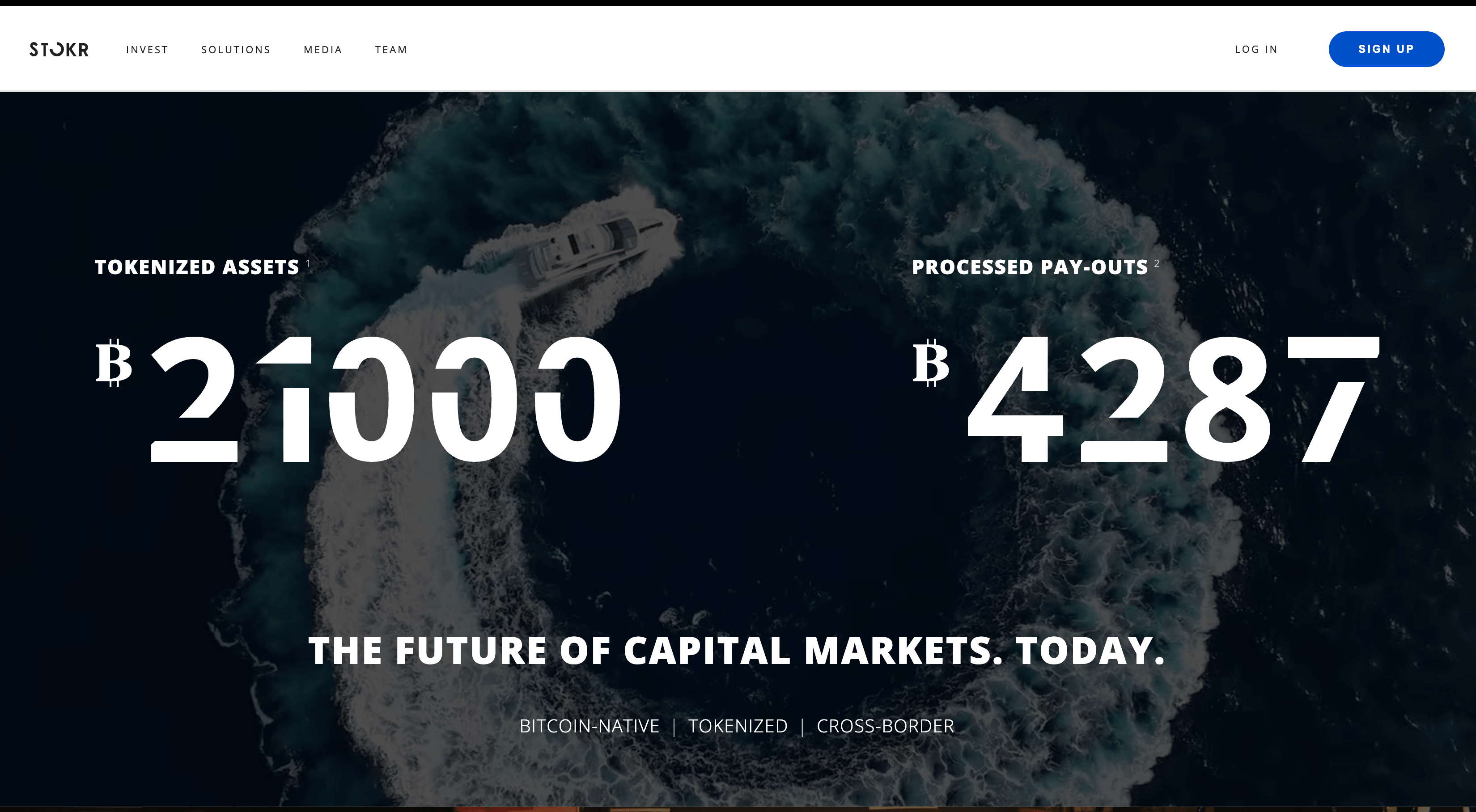

6. STOKR — Bitcoin-native tokenization on Liquid

TVL: $1.32B · HQ: Luxembourg

STOKR is the outlier in the top 6 — the only platform not built on Ethereum or a general-purpose L1/L2. STOKR issues exclusively on Liquid Network (Bitcoin’s federated sidechain by Blockstream), targeting a specific institutional thesis: regulated securities settled in Bitcoin.

Product portfolio:

- Blockstream Mining Note 2 (BMN2) — hashrate-backed structured note, ~$790M, the flagship

- CALCPB — Capital B (ex-Blockchain Group) Euronext shares tokenized 1:100

- CMSTR — MicroStrategy Nasdaq shares tokenized (first Liquid-issued security backed by Nasdaq stock)

- GSTR — Gold Stellar Ratio, tokenized AIF pairing gold exposure with BTC-backed fixed income

- Alternative investment funds (private equity, private credit)

Regulatory positioning: STOKR is a Luxembourg-registered VASP (via CSSF), issuing under EU capital markets law. Products are MiFID II eligible-investor only (professional investors + qualified non-EU, excluding US persons and Luxembourg/Germany residents). Minimum subscription/redemption typically $150,000.

Compliance model: KYC/AML whitelist via CSSF-supervised process. Notes tradable on Sideswap secondary market peer-to-peer against LBTC.

Best-fit use case: Issuers wanting Bitcoin-native settlement with regulated wrappers. Bitcoin treasury companies (Capital B, MicroStrategy) tokenizing their equity to trade against LBTC 24/7 in professional markets. Hashrate finance. Institutional gold-plus-BTC yield products.

Chains supported: Liquid Network only. No Ethereum. This is intentional — STOKR’s thesis is Bitcoin-anchored settlement, not multi-chain reach.

Recent trajectory: Appointed Subhankar Sinha (ex-BNY blockchain lead) as Senior Advisor in Q1 2026, focused on US institutional expansion and MMF tokenization. Two new digital securities live in Q1 2026 (CALCPB, CMSTR).

Why not STOKR: Single-chain (Liquid only) — if you need multi-chain distribution, STOKR is not the answer. Also, professional-investor gating with $150K minimums makes STOKR inappropriate for retail products. And Liquid’s smaller developer ecosystem vs Ethereum means fewer integration partners than any of the top 5.

Honorable mentions

Not in the top 6 by TVL, but relevant depending on use case:

- Backed Finance / xStocks ($720M) — leader in tokenized public equities. bTokens (bIB01, bCSPX, bNVDA, bTSLA, bGOOGL) are ERC-20 tracker certificates under Swiss DLT Act. Chainalysis sanctions screening on-chain. Best-fit for non-US retail access to US-listed equities. See our Backed Finance analysis in the pillar.

- Superstate ($880M) — Robert Leshner’s platform, USTB (short-duration Treasuries) and USCC (crypto-collateral fund). Tokenized IPO-tech via Opening Bell (SEC-registered equity issuance on Solana). Fast-growing challenger.

- Franklin Templeton Benji ($2.47B) — the FOBXX tokenized fund. Franklin’s own platform, not open to third-party issuers. Institutional treasury only.

- WisdomTree ($754M) — WTGXX and related MMFs. Received SEC approval for 24/7 trading + instant USDC settlement in 2026 — a regulatory milestone.

- Polymath / Polymesh — the standards pioneer that authored ERC-1400 in 2018. Runs Polymesh, a permissioned L1 for regulated securities with Confidential Assets (ZK privacy). Niche 2026 positioning; matters more for standards history than TVL leadership.

- Real estate specialists — RealT (US residential rentals, Delaware series LLC), Brickken (EU real estate under Spanish DLT law), Propy (on-chain title transfer), RedSwan CRE (US commercial real estate), Blocksquare (white-label for developers). Real estate has its own platform landscape — treasuries/credit specialists don’t cross over.

Choosing the right platform

Decision framework by use case:

| Use case | Recommended platform | Why |

|---|---|---|

| US institutional fund tokenization | Securitize | Only full regulated stack (transfer agent + broker-dealer + ATS) |

| Retail non-US treasuries | Ondo (USDY) | Blocklist compliance, permissionless composability |

| EU corporate treasury | Spiko | UCITS regulatory wrapper, MiFID II compatible, 24/7 stablecoin subscriptions |

| Private credit + DeFi collateral | Centrifuge | ERC-4626/7540 native, multi-chain hub-and-spoke |

| Institutional crypto lending | Maple | Zero losses since 2023, dual permissioned/permissionless products |

| Bitcoin-native settlement | STOKR | Liquid Network specialization, MiFID II eligible-investor gate |

| Tokenized public equities (non-US) | Backed (honorable mention) | xStocks, Chainalysis on-chain, Swiss DLT Act |

| US commercial real estate | RedSwan CRE | Reg D 506(c), institutional-grade |

| EU real estate | Brickken | Spanish DLT law, EU-regulated |

Cross-cutting questions before choosing:

- Are you the issuer or the integrator? Issuers care about regulatory scope, compliance model, and legal wrapper support. Integrators (dashboards, indexers, wallets) care about API surface, event schemas, and compliance-check interfaces.

- What jurisdictions? US only → Securitize or Ondo OUSG. Non-US retail → Ondo USDY, Backed. EU only → Spiko, STOKR, Brickken. Cross-border → dual-track Reg D + Reg S with Securitize or Centrifuge.

- What compliance tolerance for your investors? Institutional accept KYC allowlists. Retail crypto users want permissionless (Ondo USDY, Maple syrupUSDC, Centrifuge open pools).

- Which chains does your downstream infrastructure support? Most platforms are multi-chain now, but each has a home chain where liquidity concentrates. Ethereum for BUIDL, Solana for USDY, Liquid for STOKR.

The infrastructure layer

Every one of these six platforms depends on RPC infrastructure that they don’t run. The RWA workload is different from typical DeFi: compliance checks, oracle state polling, NAV updates, custodian attestation monitoring, and transfer-event indexing run continuously on schedules tied to regulatory requirements, not user activity. A failed RPC call in an RWA context isn’t a bad UX — it can be a broken compliance check or a missed settlement with legal consequences.

For teams integrating with any of these platforms — indexers, portfolio dashboards, compliance monitors, treasury tools — the practical setup is dedicated multi-chain RPC nodes with archive access, redundant WebSocket subscriptions, and SOC 2 Type II certification where the downstream product is regulated. Chainstack covers all of this through RWA-specific blockchain infrastructure.

For chain-specific setup:

- Ethereum RPC for RWA in 2026 — the default for Securitize, Centrifuge, Backed

- Solana RPC for RWA — for Ondo USDY, BUIDL on Solana, Maple

- BNB RPC for RWA — for Ondo, Backed cross-chain

- Arbitrum RPC for RWA — for institutional L2 exposure

Chainstack’s open-source rwa-sdk exposes all major compliance models (blocklist, KYC registry, sanctions screening, bitmap manager, pre-transfer check) behind a single can_transfer() interface. One call works across USDY, OUSG, BUIDL, syrupUSDC, and Backed’s bTokens.

Conclusion

The tokenization platform market consolidated in 2026. Six platforms account for the majority of distributed on-chain RWA value: Securitize for US institutional, Ondo for retail treasuries, Spiko for EU corporate, Centrifuge for DeFi-native credit, Maple for institutional lending, and STOKR for Bitcoin-native structured products.

The right choice depends on your jurisdiction, investor base, compliance tolerance, and integration ambitions. There’s no single “best” — each platform has clear best-fit use cases and honest limitations, and the ecosystem’s diversity is a strength, not a fragmentation.

Chainstack sits below all six as the RPC layer that applications depend on to read state, index events, and run compliance checks. If you’re building on top of any of these platforms:

- What is a tokenization platform? RWA leaders, standards & compliance in 2026 — the pillar guide for context

- Top 7 RWA token data tools for developers in 2026 — developer tooling

- Blockchain infrastructure for RWA — the Chainstack RWA product surface

Platform choice is the second-most important RWA decision after “what asset are we tokenizing?” Infrastructure is the third. Get the ordering right.

FAQ

Securitize, at $4.39B in RWA distributed value across 24 tokens (RWA.xyz, July 2026 snapshot). BUIDL alone — BlackRock’s tokenized money market fund managed via Securitize — accounts for most of that.

For non-US retail, Ondo Finance’s USDY — permissionless-friendly (blocklist model), 4.65% APY, available across Ethereum, Solana, and other chains. For EU retail, Spiko — UCITS-regulated, 1 EUR minimum. US retail is largely gated (Reg D 506(c) accredited-only, or OUSG’s qualified purchaser threshold).

Depends on jurisdiction. RealT for US residential rentals (Delaware series LLC). RedSwan CRE for US commercial real estate. Brickken for EU real estate under Spanish DLT law. Blocksquare for white-label infrastructure if you want to run your own tokenization stack. None of the top 6 platforms in this list is a real-estate specialist — treasury and credit dominate their focus.

Backed Finance is a tokenization platform, and xStocks is its consumer brand for tokenized equities. Backed’s TVL sits at ~$720M as of mid-2026 (RWA.xyz), which places it just outside the top 6 by pure TVL, but its secondary trading volume exceeds $20B cumulative — leadership by volume, not by TVL. Best-fit for non-US retail wanting US stock exposure.

Five of six do: Securitize, Ondo, Spiko, Centrifuge, Maple. STOKR is the exception — it issues exclusively on Liquid Network (Bitcoin’s federated sidechain) and has no Ethereum plans.

Securitize if you’re an institutional issuer bringing a fund on-chain and need transfer-agent + broker-dealer + ATS services under one roof. Ondo if you want to buy tokenized treasuries directly as an investor, or you’re a DeFi builder integrating tokenized-treasury liquidity into your protocol. They serve different sides of the market.

Yes. RWA workloads are different from typical DeFi — continuous compliance checks, oracle state polling, and event indexing run on schedules tied to regulatory requirements, not user activity. Public endpoints fail most of these under production load. Chainstack offers dedicated multi-chain RPC nodes with archive access, WebSocket stability, and SOC 2 Type II certification for regulated environments.

Additional resources

Chainstack RWA content:

- What is a tokenization platform? RWA leaders, standards & compliance in 2026

- Top 7 RWA token data tools for developers in 2026

- RPC infrastructure for RWA: EVM node requirements

- Blockchain infrastructure for RWA

Chain-specific guides:

- Ethereum RPC for RWA in 2026

- BNB RPC for RWA

- Best Arbitrum RPC providers for RWA 2026

- How to get an Ethereum RPC endpoint for RWA

- How to get a Solana RPC endpoint for RWA

Developer tools: