Ethereum

Ethereum Hyperliquid

Hyperliquid Solana

Solana Arbitrum

Arbitrum BNB Smart Chain

BNB Smart Chain Base

Base Polygon

Polygon TRON

TRON Sui

Sui MegaETH

MegaETH

What is a tokenization platform? RWA leaders, standards & compliance in 2026

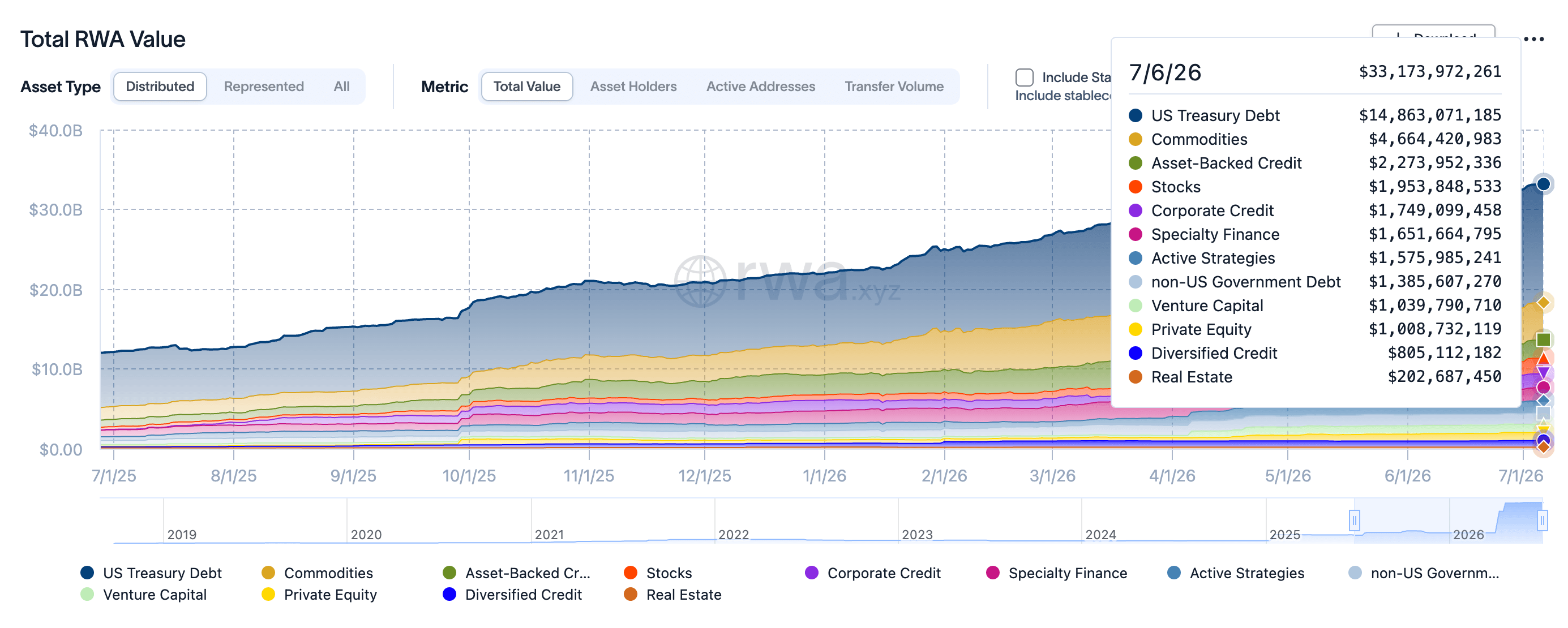

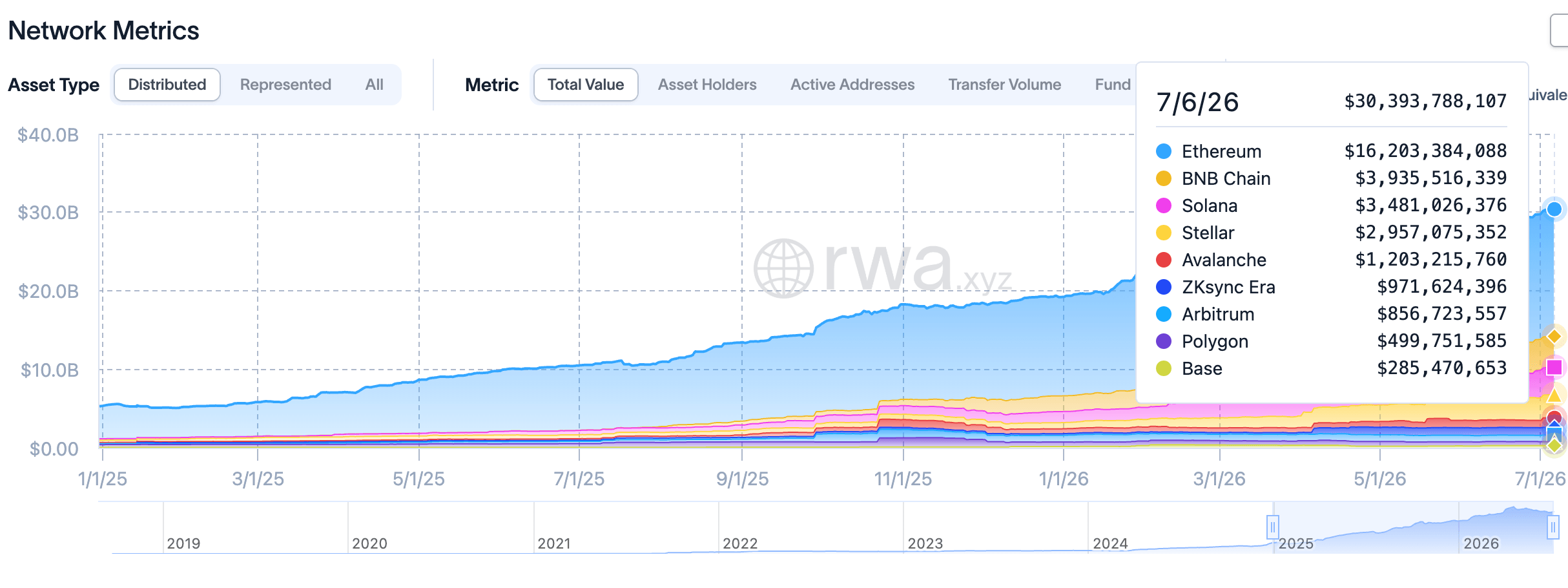

In 2026, real-world asset (RWA) tokenization stopped being a thesis and became a market. Distributed RWA value on-chain hit $30.39B in July 2026 (RWA.xyz, 7/6/2026 snapshot), up nearly fivefold from ~$6.6B a year earlier. Nearly a million holders now sit on tokenized treasuries, private credit, real estate, and equities across 38 networks and 193 issuing platforms.

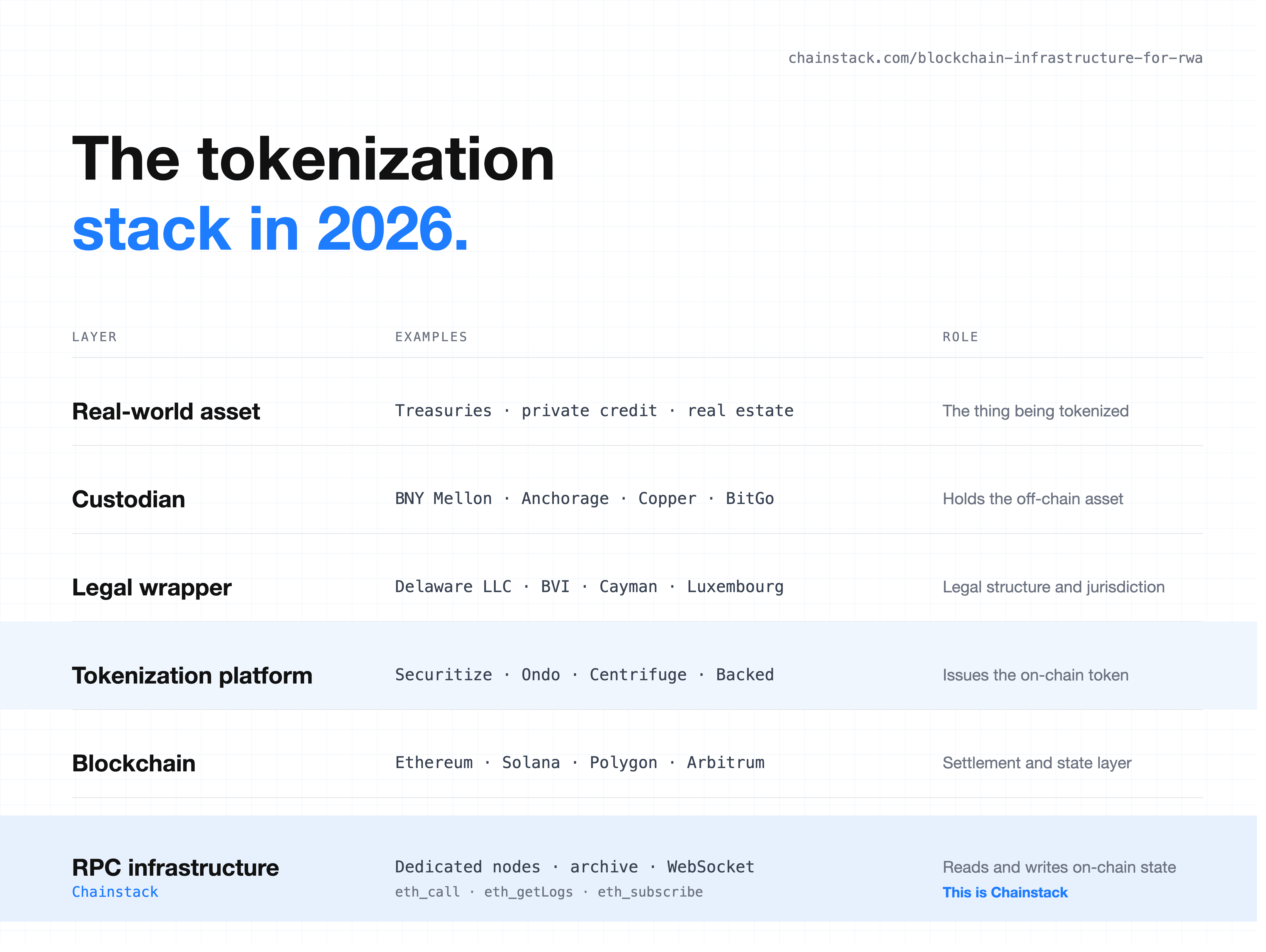

But the market is easy to misread. People conflate tokenization platforms (Securitize, Ondo, Centrifuge) with the tokens they issue (BUIDL, USDY, JTRSY) and with the infrastructure underneath (RPC nodes, oracles, custody). Three different layers. Getting them straight is the starting point.

This guide covers what a tokenization platform is, how tokenization works, the best tokenization platforms in 2026, token standards, compliance models, real estate platforms as a separate vertical, US and EU regulation including NYSE’s proposed 24/7 tokenized-securities platform, and the infrastructure layer beneath all of them.

Positioning note: Chainstack is an RPC infrastructure provider. We sit below tokenization platforms in the stack, not alongside them.

What is a tokenization platform?

A tokenization platform is the software layer that turns off-chain ownership into an on-chain token and enforces who can hold it. It converts ownership of treasuries, private credit, real estate, equities, or commodities into blockchain-native tokens that can be transferred, held, and traded programmatically, while enforcing regulatory compliance at the contract level.

What a tokenization platform does:

- Onboards the asset — legal wrapper, valuation, off-chain custody arrangement

- Issues the token — smart contract deployment, standard selection (ERC-1400, ERC-3643, ERC-4626, DS Protocol, custom)

- Enforces compliance — KYC and sanctions checks on every transfer

- Manages investors — allowlists, blocklists, jurisdictional restrictions, accreditation status

- Runs the lifecycle — dividends, coupons, NAV updates, redemptions, corporate actions

- Reports — regulatory filings, investor statements, audit trails

What a tokenization platform does not do:

- Hold the asset. The custodian does (BNY Mellon for BUIDL, Copper for Backed, Anchorage Digital).

- Run the blockchain. Ethereum, Solana, Polygon, Arbitrum, BNB Chain do.

- Provide the RPC layer. Infrastructure providers like Chainstack do.

The clean mental model: custodian holds the asset, tokenization platform issues and manages the token, blockchain settles the transfer, RPC infrastructure enables applications to read and write on-chain state.

How does tokenization work?

Tokenization runs through five steps. Skip any one and the token can’t legally be transferred.

- Legal wrapper — issuer forms an SPV to hold the asset in a bankruptcy-remote structure (Delaware LLC for US Reg D, BVI for global institutional, Cayman for offshore, Luxembourg RAIF for EU AIFs).

- Custodian arrangement — off-chain asset locked with a regulated custodian. Custodian attestations reconcile on-chain supply with off-chain reserves.

- Token standard selection — ERC-3643 for regulated securities, ERC-4626 for yield-bearing vaults, ERC-7540 for async settlement RWA, DS Protocol for Securitize, or custom implementations (Ondo). Standard choice determines every subsequent compliance and integration cost.

- Smart contract deployment — token contract plus the compliance stack (identity registry, trusted-issuers registry, compliance module). A full ERC-3643 deployment is typically 6-8 contracts. For a hands-on end-to-end walkthrough of tokenizing an asset on Ethereum, see our Ethereum asset tokenization tutorial.

- Compliance and lifecycle setup — KYC registry populated, oracle NAV feeds connected, transfer restrictions configured, minting authority assigned.

New issuance on an existing platform typically takes 4–12 weeks. Building a new legal-and-custody stack from scratch takes 6–12 months.

The 2026 RWA market in numbers

All figures from RWA.xyz‘s distributed-value methodology (07/06/2026 snapshot). The tokenized assets platform ecosystem now spans 193 issuers across 38 chains.

- Distributed RWA value (excl. stablecoins): $30.39B (as of 7/6/2026)

- Total RWA holders: 955,328 (+6.84% 30d)

- Stablecoin value (separate category): $295.36B

- Tokenized US treasuries alone: $13.4B by early April 2026, the largest single RWA vertical

DefiLlama shows a lower $28.30B onchain market cap for RWA. Gaps come from methodology (distributed value vs onchain mcap vs strict market cap; category composition changes over time), not error.

RWA value by chain (RWA.xyz, distributed value excl. stablecoins):

| Network | RWA Value | Notes |

|---|---|---|

| Ethereum | $16.20B | ~53% of the market, institutional default |

| BNB Chain | $3.94B | Deep institutional adoption in Asia |

| Solana | $3.48B | Fastest-growing large chain — $873M → $1.66B (+90%) in 30 days early 2026 |

| Stellar | $2.96B | Cross-border settlement focus |

| Avalanche | $1.20B | |

| ZKsync Era | $971.6M | Tradable private credit dominates |

| Arbitrum | $856.7M | L2 default for institutional issuers |

| Polygon | $499.8M | Low-cost EVM, broad issuer support |

| Base | $285.5M | Fast-growing L2 |

Total across all networks in the RWA.xyz distributed view: $30.39B (7/6/2026). “Distributed” means tokens move to external wallets, distinct from “represented” (blockchain used only as recordkeeping). Provenance ($19.5B) and Canton ($113B) are excluded because they sit in the recordkeeping-only bucket — investors can’t transfer those tokens.

Major tokens (mid-2026):

| Token (issuer) | Value | Chain(s) |

|---|---|---|

| BUIDL (BlackRock / Securitize) | ~$2.4–3.0B | Ethereum, Arbitrum, Polygon, Aptos, Avalanche, Optimism, Solana |

| USDY (Ondo) | ~$740M | Ethereum, Solana, Mantle, Sui, Aptos |

| OUSG (Ondo) | $407–479M | Ethereum |

| Ondo Global Markets | ~$1B (crossed May 11, 2026) | Ondo Chain testnet, Ethereum |

| ACRED (Apollo / Securitize) | ~$115M | Aptos, Avalanche, Ethereum, Ink, Polygon, Solana |

| xStocks (Backed) | ~$25–32M TVL, >$20B cumulative volume | Ethereum, Base, Arbitrum, Gnosis, more |

| JTRSY (Centrifuge) | $875.8M | Ethereum, Base, Arbitrum, Avalanche, Plume |

| syrupUSDC (Maple) | ~$1.29B | Ethereum, Base, Solana, Arbitrum |

Tokenization platforms in 2026: who’s who

Six platforms account for most on-chain RWA value distributed to external wallets. Each takes a different technical and regulatory approach.

| Platform | TVL | Key tokens | Chains | Compliance model |

|---|---|---|---|---|

| Securitize | ~$4.4B AUM (No. 1 platform, ~20% share) | BUIDL, ACRED | Ethereum, Arbitrum, Polygon, Aptos, Avalanche, Optimism, Solana | DS Protocol (proprietary, preTransferCheck) |

| Ondo Finance | ~$3.65B (USDY $740M + OUSG $407–479M + Global Markets ~$1B) | USDY, OUSG, tokenized US stocks | Ethereum, Solana, Mantle, Sui, Aptos, XRP Ledger, BNB Chain | Blocklist (USDY) + KYC registry (OUSG) |

| Centrifuge | ~$1.6B | JTRSY ($875.8M), JAAA | Ethereum, Base, Arbitrum, Avalanche, Plume, BNB Chain, Optimism | ERC-1404 + ITransferHook hooks; ERC-4626/7540 vaults |

| Backed Finance | ~$25–32M TVL, >$20B cumulative volume | xStocks (bIB01, bCSPX, bNVDA, and more) | Ethereum, Base, Arbitrum, Gnosis, Polygon, BNB Chain, Solana | Chainalysis sanctions screening at contract level |

| Maple Finance | ~$2.0–2.2B | syrupUSDC ($1.29B), syrupUSDT | Ethereum, Base, Solana, Arbitrum, Plasma | Bitmap permission manager (institutional); ERC-4626 open (syrupUSDC) |

| Polymath / Polymesh | Low public TVL — niche player | Various security tokens on Polymesh L1 | Polymesh (permissioned L1) | ERC-1400 (originator) + Confidential Assets (ZK privacy) |

Data sources: RWA.xyz (July 2026 snapshot), individual issuer disclosures.

A deeper comparison — pricing, developer integration surface, side-by-side feature matrix, best-fit use cases per platform — belongs in a dedicated listicle (Top 6 RWA tokenization platforms in 2026, published separately). This pillar covers the mechanics all six share: token standards, compliance models, and infrastructure requirements.

Beyond these six, real estate tokenization has its own specialized platform landscape — covered next.

Real estate tokenization platforms

Real estate is a major RWA vertical with a different platform landscape than treasuries or private credit. Where BlackRock and Apollo work with Securitize, real estate issuers typically use specialized platforms designed around jurisdictional property law and title-transfer complexity.

Notable real estate tokenization platforms:

- RealT — US-focused, Delaware series LLC structure for fractional single-family rentals (primarily Detroit and Cleveland). 400+ properties tokenized; investors receive daily rental income on-chain.

- Brickken — EU-regulated, Barcelona HQ. Full-stack platform for real estate, private equity, and SME funding under Spanish DLT law. Operates across Ethereum, Polygon, and BNB Chain.

- Propy — US real estate transactions on-chain, blockchain-based title tracking. Focused on tokenizing whole properties rather than fractional ownership.

- RedSwan CRE — commercial real estate tokenization for accredited US investors (multifamily, office, industrial). Reg D 506(c) issuance.

- Blocksquare — Slovenia-based, standardized fractional real estate. White-label infrastructure for real estate developers.

Real estate tokenization is legally heavier per token than treasury tokenization. Property law is jurisdiction-specific (the wrapper matters more), title transfer requires off-chain enforcement, and rental income distribution varies by platform. Tokenized real estate TVL still trails treasury tokens by roughly 10× in 2026 despite the larger addressable off-chain market.

The best real estate tokenization platform depends on jurisdiction: US residential → RealT; EU → Brickken; US commercial → RedSwan CRE; white-label for developers → Blocksquare.

Token standards that power these platforms

Compliance is enforced at the contract layer through token standards. The four that matter in 2026:

ERC-1400

Polymath’s original security-token standard. Umbrella library (ERC-1410 partitions, ERC-1594 core, ERC-1643 documents, ERC-1644 controller ops). In 2026, largely superseded by ERC-3643 as the accepted institutional standard. Concepts persist — Centrifuge uses ERC-1404 restriction compatibility, a sibling standard.

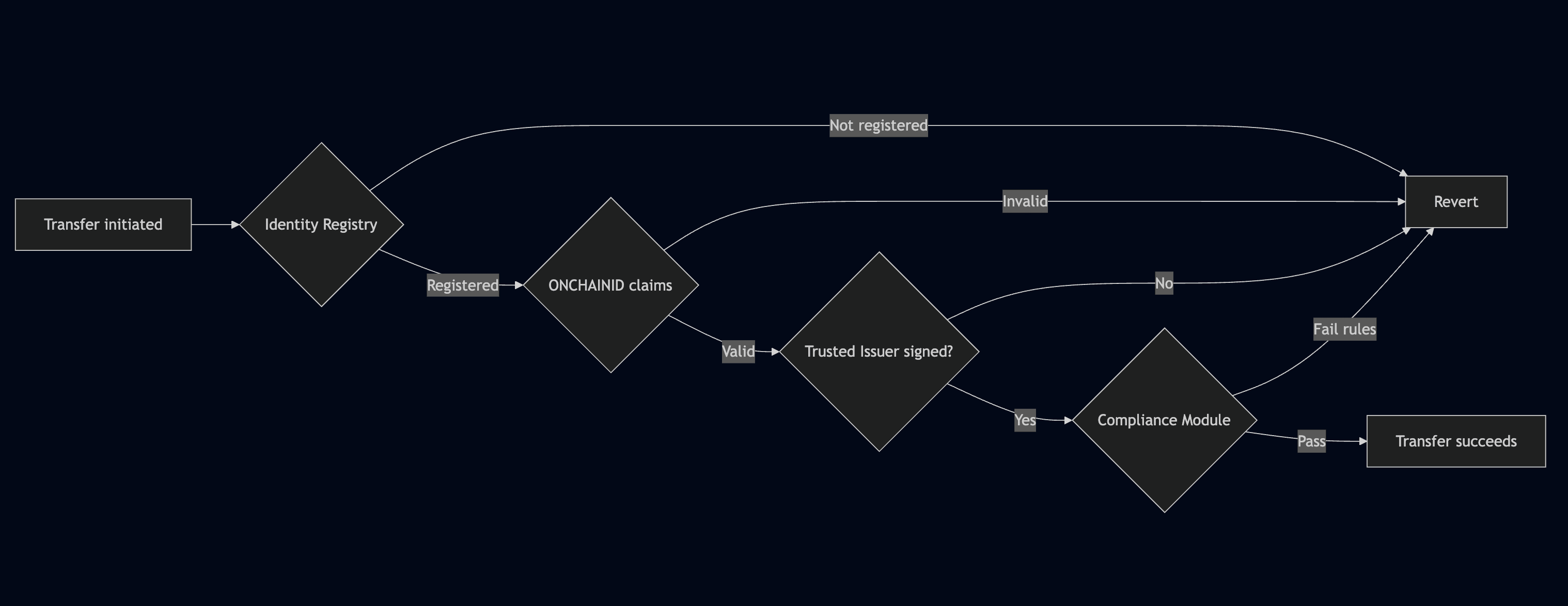

ERC-3643 (T-REX Protocol) — the de facto institutional standard

Originally designed for security tokens — the general category of tokens representing regulated securities. In 2026, “security token” and “RWA token” are used almost interchangeably in practice, since most RWA on-chain is securities. ERC-3643 has become the reference standard for securities tokenization platforms serving institutional issuers.

Created by Tokeny (Luxembourg), accepted as ERC-3643 in 2023, governed by the ERC-3643 Association (90+ members). Architecture:

- ONCHAINID — identity contract storing hashed claims (not PII), one per user

- Identity Registry — approved holders

- Trusted Issuers Registry — which KYC providers may sign which claims

- Compliance module — jurisdiction caps, accreditation, lockups, max holders

Every transfer runs: Identity Registry → ONCHAINID claims → Trusted Issuer → Compliance rules. Fail any check, transfer reverts on-chain.

ERC-20 compatible. Over $32B in tokenized assets across 180+ jurisdictions now run on ERC-3643. Recognized as the reference standard for compliant tokenized securities by industry consortia. DTCC integration underway. ISO TC 307 standardization in progress — which would make ERC-3643 the first Ethereum token standard with ISO recognition.

ERC-4626 — the vault standard

Vault shares are themselves ERC-20 tokens. Interface: deposit, mint, withdraw, redeem, plus conversion math.

Why it fits yield-bearing RWA: NAV accrues into the share exchange rate directly without rebasing. Shares are composable as collateral in Morpho, Aave, Euler, Pendle. Naive implementations are vulnerable to a first-depositor inflation attack — the OpenZeppelin variant patches this by seeding a virtual share.

Over $25–30B TVL sits in compliant ERC-4626 vaults as of April 2026. Used by Maple syrupUSDC and Centrifuge. ERC-7540 (async, finalized March 2024) extends it with requestDeposit and requestRedeem for slow-settling RWA.

DS Protocol (Securitize)

Proprietary standard, powers BUIDL. Key function to know:

function preTransferCheck(address _from, address _to, uint _value)

view public returns (uint code, string reason);

Calls the Compliance Service to simulate a transfer gaslessly, returning validity plus a reason before execution. Enforces OFAC sanctions on-chain, permits freeze, burn, and reissue. The off-chain rulebook (jurisdiction rules, holder limits) is enforced through the on-chain Compliance Service.

How compliance actually works — 5 models

Compliance isn’t one thing. Every major RWA token implements it differently. Chainstack’s open-source rwa-sdk exposes all five behind a single can_transfer() interface:

- Blocklist — Ondo USDY. Deny-list. Most permissionless-friendly, but reactive.

- KYC registry (allowlist) — Ondo OUSG. Only whitelisted addresses may hold. Limited composability.

- Chainalysis sanctions screening — Backed. Contract-level checks against live Chainalysis data.

- Bitmap permission manager — Maple institutional pools. Gas-efficient on-chain bitmap encoding eligibility. syrupUSDC vault has no gate.

- DS Protocol pre-transfer check — Securitize BUIDL.

preTransferCheck()returns validity + reason before transfer. Most comprehensive on-chain compliance stack in production.

For developers, this means a naive balanceOf / transfer flow won’t work. Every application needs to know which model each token uses. The rwa-sdk abstracts all five behind a single call:

from rwa_sdk import RWAChain

rwa = RWAChain(rpc_url="https://ethereum-mainnet.core.chainstack.com/YOUR_KEY")

# One call works across all 5 compliance models

check = rwa.can_transfer("USDY", sender, receiver)

print(check.can_transfer) # True / False

print(check.method) # ComplianceMethod.BLOCKLIST (or KYC_REGISTRY, SANCTIONS, BITMAP, PRE_TRANSFER_CHECK)

print(check.restriction_message) # "sender is on the blocklist"

Behind the call, the SDK issues an eth_call to the correct compliance contract for the token, parses the return, and normalizes the response across all 5 models. Which is why the RPC endpoint underneath matters — one dropped call means one missed compliance check. We covered the developer-facing view of RWA data tooling in Top 7 RWA token data tools for developers in 2026.

Regulation in 2026: US and EU

Regulation is the other half of what a tokenization platform enforces.

United States — Project Crypto

SEC Chairman Paul Atkins launched Project Crypto with a substantially clearer stance in late 2025 / early 2026. Key milestones:

- November 12, 2025 — Atkins “Inside Project Crypto” establishes taxonomy: digital commodities, digital collectibles, digital tools, and tokenized securities. Core principle: “tokenized securities are and will continue to be securities.”

- January 28, 2026 — Joint Staff Statement on Tokenized Securities: federal securities laws apply regardless of whether ownership is recorded on-chain or off-chain.

- March 17, 2026 — SEC interpretive release plus Atkins “Token Safe Harbor” speech proposing a startup exemption, fundraising exemption, and investment-contract safe harbor. Proposals, not final rules.

- DTC tokenization pilot — no-action letter December 11, 2025; targeted launch 2H 2026.

Exemption paths: Reg D 506(c) (US accredited), Reg S (non-US), Rule 144A / 3(c)(7) (QIBs and qualified purchasers). Secondary trading through ATS operators like Securitize Markets.

NYSE’s tokenized securities platform

In January 2026, NYSE announced plans for a 24/7 tokenized-securities platform with stablecoin-based settlement, stating it will seek regulatory approvals to launch the venue — the first traditional US exchange to publicly commit to an always-on tokenized-securities trading venue.

Nasdaq’s parallel filing with the SEC — a formal SRO rule change proposal, not just an announcement — takes a more conservative approach: T+1 settlement, business hours only. NYSE’s regulatory path is still to come; Nasdaq’s is in review as of mid-2026.

If approved, NYSE’s tokenized securities platform would be a structural shift for institutional issuers — a regulated US exchange operating around the clock with stablecoin settlement changes the calculus for issuers currently choosing between Securitize Markets and traditional listing venues.

European Union — MiCA

MiCA (Regulation EU 2023/1114) is now in full effect. Timeline: ART/EMT rules took effect June 30, 2024; CASP authorization from December 30, 2024; grandfathering to July 1, 2026. 53+ CASP licenses granted by November 2025.

Three categories: ARTs (basket-backed), EMTs (single-fiat-pegged, no interest allowed), and other crypto-assets.

The most important MiCA fact for RWA: it’s a residual regime. Tokens qualifying as MiFID II financial instruments (most tokenized securities, tokenized funds, tokenized bonds, tokenized real-estate equity) stay under MiFID II, Prospectus Regulation, UCITS, and AIFMD — NOT MiCA (Article 2(4); ESMA’s December 2024 qualification guidelines are controlling).

If you’re issuing a tokenized bond in the EU, MiCA is not your primary framework. MiFID II is. MiCA covers what falls outside MiFID II.

For piloting secondary-market infrastructure specifically, the DLT Pilot Regime (Regulation 2022/858, €6B cap) enables tokenized-securities trading venues — 21X in Germany is one live example.

Dual-track (US + EU) at the same time

Platforms serving both jurisdictions run dual-track structures: Reg D for US accredited plus Reg S for non-US, with the token contract enforcing the eligibility split at the wallet level. Ondo’s USDY (non-US) and OUSG (US qualified purchasers) is the archetype.

For EU issuers, the first legal question is always: is this token a MiFID II financial instrument, or does it fall under MiCA? The answer determines the entire compliance stack.

Choosing a blockchain

Chain choice is an infrastructure decision, not just a TVL or fee decision. Each chain imposes distinct RPC and archive requirements on the platform.

| Chain | RWA value | Notable issuers | Technical profile |

|---|---|---|---|

| Ethereum | $16.20B | BUIDL, Securitize, Ondo | Institutional default; heaviest infrastructure (archive + eth_getLogs at scale). See Ethereum RPC for RWA. |

| BNB Chain | $3.94B | Hashnote, BlackRock, VanEck | eth_getLogs disabled on most public endpoints — dedicated RPC mandatory from day one. See BNB RPC for RWA. |

| Solana | $3.48B | BUIDL, USDY, ACRED | 400ms finality, <$0.01 fees. Grew $873M → $1.66B (+90%) in 30 days early 2026. Uses associated token accounts rather than balance mappings — a different mental model from EVM chains. See Solana RPC for RWA. |

| Arbitrum | $856.7M | Securitize, Spiko, WisdomTree | Full EVM at L2 cost; sequencer + L1 finality — track l1BlockNumber. See Arbitrum RPC for RWA. |

| Polygon | $499.8M | OUSG, ACRED, Backed | Low-cost EVM, broad issuer support. |

Robert Leshner, CEO of Superstate, in the RedStone Solana RWA Report (September 2025): “For RWAs there are really only 2 places: It’s either Ethereum or Solana.” That view is common but selective: BNB Chain’s $3.94B and Stellar’s $2.96B represent real issuer bases outside the Ethereum-Solana axis.

Each chain has a distinct operational profile. We covered per-chain requirements in RPC infrastructure for RWA: EVM node requirements.

Custody and legal wrappers

Custodians and legal wrappers sit outside the platform but define what the platform can tokenize. A Delaware LLC issuing to US accredited investors produces one design. A Cayman feeder for non-US institutional gives you another. The platform enforces the difference on-chain.

Common custodians: BNY Mellon (BUIDL), Anchorage Digital, BitGo Trust, Coinbase Custody, Fireblocks (custody-only, not tokenization), Copper (Backed), State Street.

Standard legal wrappers:

- Delaware LLC/LP — US Reg D 506(c)

- BVI business company — BUIDL is domiciled here

- Cayman exempted company/LP — institutional funds, Reg S

- Luxembourg RAIF/SICAV-RAIF — EU AIF wrappers; ELTIF 2.0 opens semi-retail access

- Master-feeder structures for cross-border funds

Rule of thumb: the wrapper matches the investor base. US accredited → Delaware. Non-US institutional → Cayman or Luxembourg. Mixed → dual-track with the token contract enforcing the split at the wallet level.

The infrastructure layer beneath every platform

Every tokenization platform depends on infrastructure it doesn’t run. That’s the RPC layer.

The RWA workload is different from typical DeFi. DeFi apps generate RPC load in proportion to transaction volume. RWA protocols run continuous background workloads (compliance checks, oracle state polling, custodian attestation monitoring, transfer event indexing) on schedules tied to regulatory and operational requirements, not user activity. A tokenized treasury fund generates the same RPC load at 2am Sunday as at peak trading hours.

A failed RPC call in an RWA context isn’t a bad UX. It can be a broken compliance check or a missed settlement with legal consequences.

RPC methods that matter most for RWA:

eth_call— synchronous compliance simulation against ERC-1400 / ERC-3643 identity registries on every transfer attempt. Also what Chainstack’s rwa-sdk uses.eth_getLogs— event indexing forTransfer,ComplianceCheck,OracleUpdate. ERC-3643 has a split-tracking problem: token contract and identity registry are separate on-chain components, both need independent monitoring. Disabled on most public BNB Chain endpoints.- Archive access —

eth_getStorageAtfor NAV reconstruction,debug_traceTransactionfor regulator audit trails. See archive nodes on Chainstack. - WebSocket

eth_subscribe— must stay live with auto-reconnect. Dropped subscription = missed compliance events with legal implications. - Multi-chain coverage — BUIDL is live on 4+ chains simultaneously. Maple and Centrifuge span multiple EVM chains via CCIP.

Real bottlenecks to plan for:

- NAV and oracle updates are pushed once daily or weekly for private credit and real estate. The requirement isn’t high frequency, it’s guaranteed delivery in a narrow window. If the RPC connection drops during the one window a custodian pushes NAV, the fund becomes untradable until state is corrected.

- A missed

Transferevent corrupts your view of ownership. Being wrong for even ten minutes is ten minutes of potential illegal transfers with no real-time recourse.

For teams building on tokenization platforms — indexers, portfolio dashboards, compliance monitors, treasury tools — the practical setup is dedicated multi-chain RPC nodes with archive access, redundant WebSocket subscriptions, and SOC 2 Type II certification where the downstream product is regulated. Chainstack covers all of this through RWA-specific blockchain infrastructure. Chain-specific setup: How to get an Ethereum RPC endpoint for RWA.

Conclusion

The market spent 2024 arguing whether tokenization was real. In 2026, that argument is over. The question is which layer of the stack you build on, and which one you outsource.

$30.39B is distributed on-chain. Nearly a million holders. Six leading tokenization platforms accounting for most of the value (with a deep-dive comparison coming in a separate listicle). A separate real estate tokenization vertical with its own specialized platforms. Five distinct compliance models. A US and EU regulatory landscape clear enough to build on, with NYSE’s proposed 24/7 tokenized-securities platform potentially reshaping how institutional issuers think about listing venues.

Chainstack sits below all of this as the RPC and node layer applications actually depend on to read state, index events, and run compliance checks. If you’re evaluating platforms, comparing chains, or building on top of an existing RWA token:

- Top 7 RWA token data tools for developers in 2026 — the developer-tooling landscape

- RPC infrastructure for RWA: EVM node requirements — chain-by-chain RPC and archive requirements

- Blockchain infrastructure for RWA — the Chainstack RWA product surface

Platform, chain, infrastructure. Get all three right. The last one is where most teams under-invest, and it’s where regulated products fail first.

FAQ

A stablecoin issuer (Circle, Tether, Paxos) tokenizes one thing — fiat currency — with a fixed 1:1 peg. A tokenization platform is general-purpose middleware that can wrap treasuries, private credit, equities, real estate, or commodities. Some overlap exists: Ondo’s USDY looks stablecoin-like but is technically a yield-bearing secured note under Reg S, not a payment stablecoin.

No. Platforms don’t take custody. The underlying asset is held by a regulated custodian (BNY Mellon for BUIDL, Copper for Backed, Anchorage for the token leg of several products). The platform issues and manages the on-chain representation and enforces compliance at the contract level.

Securitize, at ~$4.4B platform asset value as of July 2026 (RWA.xyz). BUIDL alone accounts for most of that.

Technically possible, but the regulated stack is heavy. Securitize’s edge isn’t the smart contract — it’s being an SEC-registered transfer agent, broker-dealer, ATS operator, investment adviser, and fund administrator simultaneously. Most new entrants partner with existing licensed platforms. For specific verticals (real estate, private credit), specialized platforms like Brickken or Centrifuge often offer white-label options.

Depends on jurisdiction and asset type. RealT leads for US residential rentals with a Delaware series LLC structure. Brickken leads for EU real estate under Spanish DLT law. RedSwan CRE leads for US commercial real estate. Blocksquare offers white-label infrastructure. No single “best” — the right choice depends on where the property is located.

Yes. In the US, tokenized securities are securities and subject to federal securities laws — the SEC’s January 28, 2026 Joint Staff Statement is explicit. In the EU, most tokenized securities fall under MiFID II rather than MiCA. Tokenization changes the settlement mechanism, not the regulatory classification.

You need an RPC provider that supports the RWA workload profile: reliable eth_call for compliance checks, eth_getLogs at scale for event indexing (including on chains like BNB where it’s restricted on public endpoints), archive access for NAV history and audit trails, and stable WebSocket subscriptions. Public endpoints fail most of these under production load. Chainstack offers all of the above with SOC 2 Type II certification for regulated environments.

Additional resources

Chainstack RWA content:

- Top 7 RWA token data tools for developers in 2026

- RPC infrastructure for RWA: EVM node requirements

- Blockchain infrastructure for RWA

Chain-specific RPC guides for RWA:

- Ethereum RPC for RWA in 2026

- BNB RPC for RWA: best providers and infrastructure guide 2026

- Best Arbitrum RPC providers and infrastructure guide for RWA 2026

- How to get an Ethereum RPC endpoint for RWA in 2026

- How to get a Solana RPC endpoint for RWA in 2026

Hands-on tutorials:

- Ethereum asset tokenization with Embark — full end-to-end walkthrough

- Solana program derived addresses and cross-program invocations — associated token accounts for Solana RWA developers

- Chainstack

rwa-sdkon GitHub — open-source Python SDK covering all 5 compliance models

Authoritative external sources:

- RWA.xyz — primary data source for on-chain RWA value tracking

- DefiLlama RWA category — cross-verification for TVL figures

- SEC Joint Staff Statement on Tokenized Securities (January 28, 2026) — US regulatory position

- ERC-3643 T-REX Protocol — technical spec and reference implementation

- MiCA Regulation (EU 2023/1114) — EU crypto-asset framework