Hyperliquid is the fastest-growing on-chain exchange in crypto history — $6B+ in daily perp volume as of May 2026, a fully on-chain CLOB running at 200,000 orders per second, and now, as of May 2, 2026, a prediction market primitive built directly into the same matching engine. Polymarket is the opposite story: born in 2020 as a standalone prediction market, it has processed over $21.5B in volume in 2025 alone and raised at an $8B valuation with NYSE as a strategic backer. These two platforms have just become direct competitors.

HIP-4 — Hyperliquid Improvement Proposal 4 — went live on mainnet the same week Bloomberg reported Polymarket was pursuing CFTC approval to re-enter the US market. The timing is not a coincidence. The prediction market category is exploding: industry-wide monthly volume hit $21B by mid-2026, and both platforms are racing to own the infrastructure layer underneath it. What makes this comparison genuinely interesting is that HIP-4 is not a separate product — it is a new primitive on the same engine where traders already run perpetual futures and spot. That composability changes the economics in ways that Polymarket’s isolated CTF token model simply cannot replicate.

This guide breaks down what HIP-4 actually is, how Polymarket works under the hood, where the two differ on fees, resolution, liquidity, and composability, and which platform fits which workload.

Hyperliquid HIP-4 explained: what it is and how it works

HIP-4 was announced February 2, 2026 — HYPE rallied 10% on the day — co-authored by Bedlam Research and John Wang (Head of Crypto at Kalshi). It launched on testnet the same week and went live on mainnet May 2, 2026.

📖 New to Hyperliquid’s proposal system? Hyperliquid HIPs explained: HIP-1 to HIP-4 covers the full governance arc.

The formal definition from the Hyperliquid docs: outcomes are fully collateralized contracts that settle within a fixed range. They are a general-purpose primitive useful for prediction markets and bounded options-like instruments.

In plain terms: a HIP-4 outcome contract is a binary YES/NO instrument tied to a discrete event, trading between 0.001 and 0.999, with the price representing the implied probability. If you buy YES at 0.62, you profit 0.38 if the event occurs and lose 0.62 if it does not. No leverage, no liquidations. Settlement is in USDH, Hyperliquid’s native stablecoin backed by BlackRock-managed reserves and custodied by JPMorgan.

The lifecycle of a HIP-4 market

Every outcome market passes through four phases:

- Deployment — a canonical market (Phase 1) or builder-deployed market (Phase 2) is registered with the validator set, including the oracle specification, settlement time, and event description encoded in the

descriptionfield. - Opening auction — roughly 15 minutes of single-price clearing before continuous trading begins. This is where initial price discovery happens without a market maker.

- Continuous CLOB trading — the outcome book goes live on the same matching engine as perps and spot. The same maker/taker order types (GTC, ALO, IOC) apply. Outcome volume counts toward protocol-wide fee tier calculations.

- Oracle settlement and slot recycling — the authorized oracle posts a 0/1 result. For the first canonical market (recurring daily BTC binary), the oracle is Hyperliquid’s own BTC mark price. An optional challenge window exists. After settlement, the slot is recycled for the next market in the series.

Fee structure

The fee design is deliberately asymmetric compared to Polymarket:

- Zero fees to open or mint an outcome position

- Fees apply only on close, burn, or settlement

- Makers receive no rebates on outcome books (unlike perp and spot books)

- Users with aligned quote tokens (HYPE staking) get 20% lower taker fees

- Outcome volume counts toward protocol-wide tier calculations, compounding savings on perps for active prediction-market traders

The first canonical market opened May 2 with a daily BTC binary: “BTC above $78,213 on May 3 at 06:00 UTC?” — opening probability 62%, first-hours volume $54,026, OI $79,938.

The builder economy (Phase 2)

Phase 1 is curated canonical markets approved by the validator set. Phase 2 opens permissionless deployment: builders stake 1,000,000 HYPE per slot (slashable, with burned tokens for oracle manipulation or invalid state transitions). One slot recycles across many sequential markets in a series, so the economics work for teams running 20+ recurring markets per quarter.

Builders can set up to 50% additional fee share above the protocol base. Frontends at launch include Outcomexyz, Stratium, hip4.io, and the loris.tools dashboard suite.

How to query HIP-4 markets

# Fetch all live outcome markets and their metadata

curl -X POST https://api.hyperliquid.xyz/info \

-H "Content-Type: application/json" \

-d '{"type": "outcomeMeta"}'

Response structure:

{

"outcomes": [

{

"outcome": 123,

"name": "Recurring",

"description": "class:priceBinary|underlying:BTC|expiry:20260503-0600|targetPrice:78213|period:1d",

"sideSpecs": [

{ "name": "Yes" },

{ "name": "No" }

]

}

]

}

The description field encodes the full contract spec. Asset IDs for outcome trading are derived from outcomeId + binary side, documented under for-developers/api/asset-ids in the Hyperliquid docs.

Placing an order on a HIP-4 market (Python SDK)

from hyperliquid.exchange import Exchange

from hyperliquid.info import Info

from hyperliquid.utils import constants

import eth_account

# Load wallet

wallet = eth_account.Account.from_key(PRIVATE_KEY)

info = Info(constants.MAINNET_API_URL, skip_ws=True)

exchange = Exchange(wallet, constants.MAINNET_API_URL)

# Query outcome metadata to get the asset index

meta = info.post("/info", {"type": "outcomeMeta"})

outcome_asset_id = meta["outcomes"][0]["outcome"] # map to asset index per docs

# Place a limit buy of YES shares at 0.62 implied probability

result = exchange.order(

"BTC-OUTCOME-YES", # use the mapped asset name from outcomeMeta

True, # is_buy = True

100, # size (shares)

0.62, # limit price (= 62% implied probability)

{"limit": {"tif": "Gtc"}}

)

print(result)

The raw exchange-endpoint payload uses the same schema as perps — a (asset index), b (isBuy), p (price), s (size), t (order type) — signed via EIP-712:

{

"action": {

"type": "order",

"orders": [

{ "a": 123, "b": true, "p": "0.62", "s": "100",

"r": false, "t": { "limit": { "tif": "Gtc" } } }

],

"grouping": "na"

},

"nonce": 1746200000000,

"signature": { "r": "0x...", "s": "0x...", "v": 27 }

}

Polymarket explained: how it works

Polymarket runs a hybrid CLOB on Polygon. Outcome shares are Gnosis Conditional Token Framework (CTF) ERC-1155 tokens — every YES/NO pair is fully backed by exactly $1 of pUSD (post-V2) locked in the CTF contract. The CLOB itself matches off-chain (Polymarket-operated), with settlement and token transfers happening on-chain.

📖 Going deeper on Polymarket’s API? Polymarket API for developers: Gamma API, data, and Polygon RPC covers the full stack — CLOB, CTF, UMA resolution, and how to query markets programmatically with Polygon RPC.

Multi-outcome events use the NegRisk CTF adapter: a NO token in any market can be converted into one YES token across every other mutually-exclusive market plus residual collateral. This is capital-efficient for election-style markets with many candidates — a mechanism HIP-4’s binary-only Phase 1 does not yet offer.

Resolution via UMA Optimistic Oracle

Every Polymarket event resolves through the UMA Optimistic Oracle v2 via the open-source UmaCtfAdapter contract:

- A proposer posts an answer with a $750 USDC bond

- If undisputed during the 2-hour challenge window, the answer finalizes

- If disputed once, a fresh request is created (to neutralize griefing attempts)

- If disputed twice, the question escalates to UMA’s Data Verification Mechanism — a commit-reveal vote by UMA token-holders, resolving in 48–72 hours

Polymarket also uses Chainlink Data Streams for fast crypto-resolved markets (BTC price at expiry, ETH price at date) and an internal Markets Team for ruleset clarifications. The UMA DVM has processed hundreds of contested markets; the optimistic layer resolves ~98.5% of requests without escalation.

Querying Polymarket markets and placing orders (CLOB V2)

from py_clob_client.client import ClobClient

from py_clob_client.clob_types import OrderArgs, OrderType

from py_clob_client.order_builder.constants import BUY

HOST = "https://clob.polymarket.com"

CHAIN_ID = 137 # Polygon mainnet

client = ClobClient(

HOST,

key=PRIVATE_KEY,

chain_id=CHAIN_ID,

signature_type=1, # 1 = proxy wallet (Magic/email login)

funder=PROXY_FUNDER # address holding the pUSD collateral

)

client.set_api_creds(client.create_or_derive_api_creds())

# Read market data

token_id = "<yes-token-id-from-gamma-api>"

mid = client.get_midpoint(token_id)

price = client.get_price(token_id, side="BUY")

book = client.get_order_book(token_id)

print(f"Mid: {mid}, Ask: {price}")

# Place a GTC limit buy of 5 shares at $0.63

order = OrderArgs(token_id=token_id, price=0.63, size=5.0, side=BUY)

signed = client.create_order(order)

resp = client.post_order(signed, OrderType.GTC)

print(resp)

Polymarket’s API surface has four hosts: clob.polymarket.com (order entry + book), data-api.polymarket.com (positions, fills, history), gamma-api.polymarket.com (market and event discovery), and wss://ws-subscriptions-clob.polymarket.com (real-time fills and book updates). Authentication is two-tier: L1 = EIP-712 with private key, L2 = HMAC-SHA256 over API credentials derived from L1.

Splitting USDC into YES + NO tokens on-chain

// Split 100 pUSD into 100 YES + 100 NO conditional tokens

// Required for two-sided market making

await ctfContract.splitPosition(

collateralToken, // pUSD token address on Polygon

parentCollectionId, // bytes32(0) for top-level binary markets

conditionId, // from market.tokens metadata in Gamma API

[1, 2], // partition: YES = 0b01, NO = 0b10

ethers.parseUnits("100", 6) // 100 pUSD in 6-decimal units

);

HIP-4 vs Polymarket: side-by-side comparison

The table below summarizes public positioning as of May 2026.

| Feature | HIP-4 (Hyperliquid) | Polymarket |

|---|---|---|

| Live status | Mainnet May 2, 2026; Phase 1 canonical only | Mature; CLOB V2 since April 2026 |

| Architecture | Native on-chain CLOB on HyperCore | Off-chain matching, on-chain CTF settlement on Polygon |

| Market creation | Validator-curated (Phase 1); permissionless with 1M HYPE stake (Phase 2) | Permissioned — Polymarket Markets Team |

| Resolution | Authorized oracle posts 0/1; BTC mark price for first market | UMA Optimistic Oracle + Chainlink Data Streams + Markets Team |

| Collateral | USDH | pUSD (post-V2) |

| Fee on open | Zero | Zero on most markets; 1.56–1.80% peak taker on 15-min crypto markets |

| Fee on settle | Yes — fees apply on close/burn/settle | Zero — winning shares redeem $1.00 |

| Maker rebates | None on outcome books | Daily USDC rebates funded by taker fees |

| Cross-margin | Unified margin with perps and spot | None — isolated to Polymarket |

| Multi-outcome | Binary only in Phase 1 | NegRisk adapter for multi-candidate events |

| Throughput | Shared 200k orders/sec matching engine | Limited by Polygon + off-chain matching |

| On-chain matching | Fully on-chain CLOB | Off-chain matching, on-chain settlement only |

| DeFi composability | HyperEVM can read outcome state; vault integration possible | CTF ERC-1155s technically composable but ecosystem support thin |

| US access | Geo-blocked | International platform blocked; US-licensed arm pending |

| Market breadth | Crypto price binaries only today | Politics, sports, geopolitics, macro, pop culture |

Choose by use case

For delta-neutral crypto strategies and perp hedging

A trader long ETH-PERP facing binary event risk (Fed decision, CPI release, on-chain governance vote) has historically had two options: reduce the position or accept the binary exposure. HIP-4 introduces a third option: buy a YES or NO contract on the same event, in the same margin account, with no additional collateral requirement. The outcome position partially offsets the perp’s directional risk without unwinding it.

The mechanics work because HIP-4 positions are 1× isolated with no liquidation — the maximum loss is the entry premium — and because Hyperliquid’s margin engine aggregates across all positions. A $10,000 ETH-PERP long plus $1,000 in BTC-DOWN YES contracts is one portfolio, not two accounts. For traders already running on Hyperliquid, the cost of entry to prediction markets is near-zero. For Polymarket users, this use case is simply unavailable — Polymarket has no perp layer and no cross-margin mechanism.

For prediction market arbitrage between HIP-4 and Polymarket

Both platforms now run overlapping crypto binary markets. Polymarket’s 15-minute BTC markets charge up to 1.56–1.80% peak taker fees (at 50% probability). HIP-4 charges zero on open. A bot that simultaneously quotes on Polymarket and takes on HIP-4 (or vice versa) has a structural edge every time the two platforms misprice the same underlying event.

The technical requirements for this strategy: sub-second latency to both CLOBs, simultaneous WebSocket subscriptions to both order books, position management across Polygon (Polymarket) and HyperCore (HIP-4), and collateral bridging logic (pUSD on Polygon vs. USDH on Hyperliquid). The engineering is non-trivial but the fee asymmetry is durable — it exists by design, not accident, and will persist through Phase 1 at minimum.

For political, sports, and qualitative event markets

This is Polymarket’s home territory and it is not close. The “Will the US strike Iran?” market hit $73M in February 2026. MLB’s exclusive Official Prediction Market Exchange partnership (March 2026) gives Polymarket proprietary real-time Sportradar data for baseball markets. Geopolitics, awards ceremonies, economic indicators, central bank decisions with qualitative outcomes — these all require UMA’s arbitrary-truth resolution machinery. HIP-4’s Phase 1 oracle is Hyperliquid’s own BTC mark price. It cannot resolve “Did Kamala Harris win the Iowa caucus?” until Phase 2 deploys a politically-verified oracle with appropriate dispute mechanisms.

For any user whose primary interest is non-crypto prediction markets, Polymarket is the only serious option today. The question is whether Phase 2’s permissionless builder economy changes this — and that answer depends on which external oracle networks builders integrate with first.

Platform breakdown

Hyperliquid HIP-4

Hyperliquid’s HIP-4 launched with deliberate constraints. The first canonical market is a recurring daily BTC binary — arguably the simplest possible prediction market, one where the oracle is trivially verifiable (Hyperliquid’s own published BTC mark price) and the resolution is unambiguous. This is a sound engineering choice: launch the narrowest possible market, prove oracle reliability, then expand.

The infrastructure story is the actual differentiator. Because outcome books live on HyperCore alongside perp and spot books, every piece of trading infrastructure already built for Hyperliquid extends to HIP-4 with minimal modification. Market-makers with existing quote generation, risk management, and hedging logic on Hyperliquid perps can extend to outcome markets at near-zero marginal cost.

The HYPE token alignment deserves mention: 97% of protocol fees across all products (including HIP-4) fund HYPE buybacks. This means every outcome market trade is directly accretive to HYPE holders — a flywheel that has no equivalent in Polymarket’s current tokenless structure (a $POLY launch is widely rumored; Gate.io’s pre-market equity contract implied a Polymarket valuation of ~$14B in April 2026 — consistent with the $8B valuation from October 2025 and the $600M round in March 2026).

Limitations: Phase 1 is limited to crypto price binaries. No maker rebates on outcome books is a deliberate choice that disadvantages pure prediction-market LPs who cannot spread infrastructure costs across perp/spot. The oracle design for non-crypto events is entirely unspecified — the Phase 2 builder stake (1,000,000 HYPE, ~$40M at recent prices) creates accountability but not a resolution methodology. US traders are geo-blocked.

Fit by workload:

- Delta-neutral crypto hedging: Excellent — unified margin is the defining advantage

- Crypto price arbitrage vs. Polymarket: Excellent — zero open fees create structural edge

- Political/sports/macro markets: Limited — Phase 1 oracle cannot resolve qualitative events

Polymarket

Polymarket is the market leader by every measurable metric: volume ($21.5B in 2025, $25.7B in March 2026 alone), user count (~840k monthly active wallets by Feb 2026), institutional backing (ICE/NYSE strategic investment at $8B valuation October 2025, $600M direct equity round March 2026), and regulatory positioning (QCEX acquisition gives a CFTC-licensed US exchange; CFTC re-entry discussions ongoing per Bloomberg April 2026).

The UMA resolution system has processed tens of thousands of markets across every conceivable event category. The ~98.5% optimistic-layer resolution rate means most markets settle without dispute; the DVM escalation path handles edge cases with a documented, token-holder-voted process. Only one market in Polymarket’s history (Barron Trump / DJT) was ever overridden by Polymarket’s internal team — a track record that supports a trust claim that HIP-4 cannot yet make.

CLOB V2 (launched late April 2026) introduced pUSD as the native collateral, new SDK requirements (upgrade to v2 packages, EIP-712 signing changes), tiered fees by market category (crypto 7.2%, sports 3%, finance/politics/tech 4%), and a maker rebate program funded by taker fees. The dynamic fee structure on 15-minute crypto markets specifically — peaking at 1.56–1.80% taker at 50% probability — is a direct response to latency arbitrage, and the design explicitly accepts that sophisticated traders will find it cheaper to trade crypto binaries on HIP-4.

Limitations: No cross-margin composability with any other DeFi primitive. The maker rebate system incentivizes LPs but the off-chain matching engine means the order book is less transparent than HIP-4’s fully on-chain CLOB. US traders on the main platform remain geo-blocked (a separate US-licensed platform via QCEX is in development). The CTF token model isolates capital — you cannot use a YES token as collateral for anything else.

Fit by workload:

- Political/sports/macro events: Excellent — depth, breadth, and UMA resolution are unmatched

- Retail prediction markets (non-crypto): Excellent — 60-second onboarding via MoonPay/Stripe fiat, no wallet required

- Delta-neutral crypto hedging: Limited — no perp layer, no cross-margin mechanism

Getting started with Hyperliquid on Chainstack

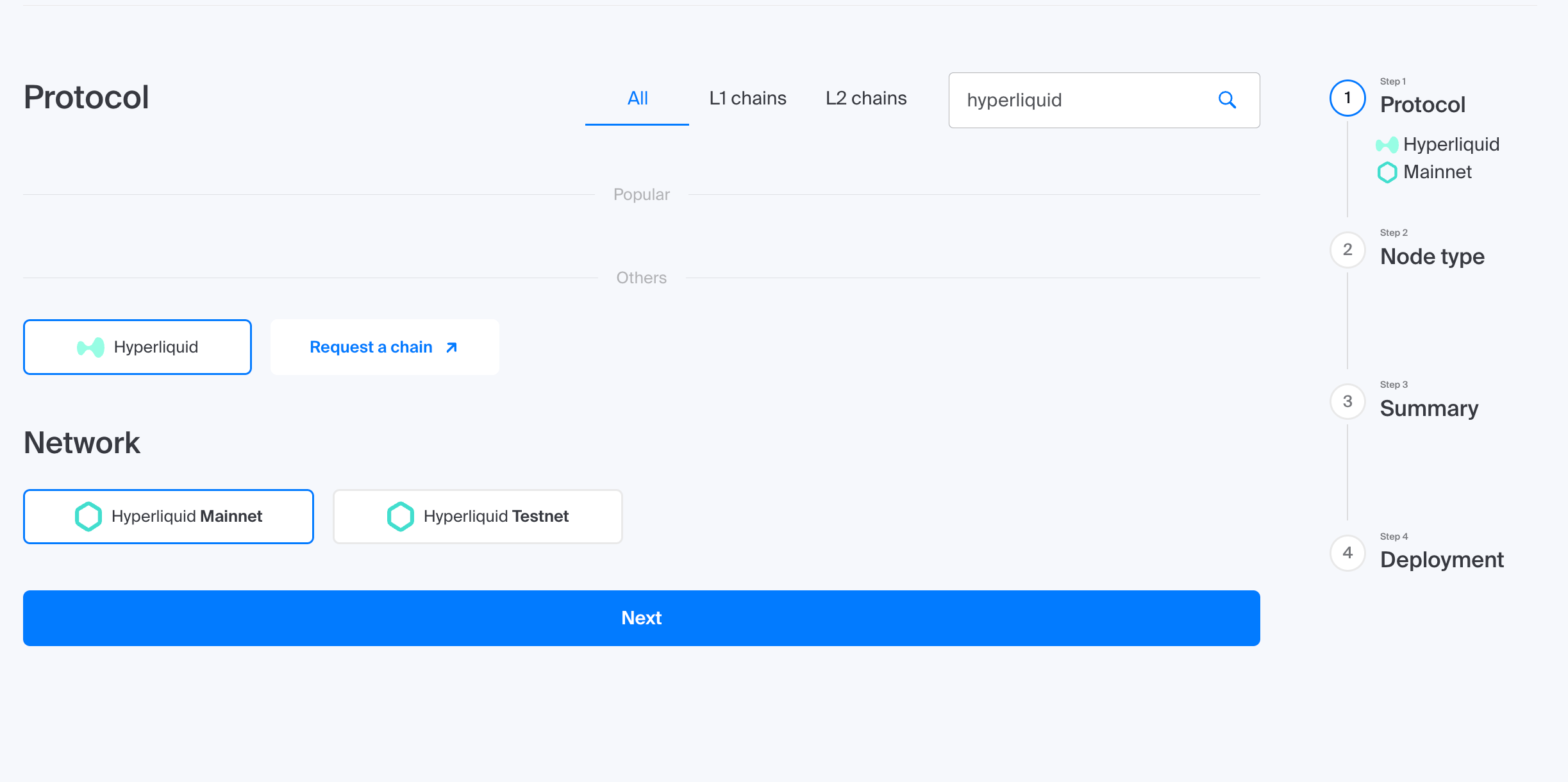

If you are building on HIP-4 — whether a market-making bot, an arbitrage strategy, a HyperEVM vault contract, or an analytics dashboard — the production infrastructure path is:

- Log in to Chainstack console (or create a free account — no card required, 3M RU/month on the Developer plan)

- Create a new project and select Hyperliquid Mainnet

- Deploy a Global Node for shared-endpoint access

- Or deploy a Dedicated Node for unlimited throughput, WebSocket streaming, and no rate limits (recommended for production bots)

- Copy your HTTP or WebSocket endpoint — it’s a drop-in replacement for the public

api.hyperliquid.xyzendpoint

Discover live outcome markets:

python

import requests

ENDPOINT = "YOUR_CHAINSTACK_ENDPOINT"

resp = requests.post(ENDPOINT, json={"type": "outcomeMeta"})

for o in resp.json()["outcomes"]:

outcome_id = o["outcome"]

yes_coin = f"#{10 * outcome_id + 0}" # e.g. "#10" for BTC daily YES

no_coin = f"#{10 * outcome_id + 1}" # e.g. "#11" for BTC daily NO

print(o["description"], "→", yes_coin, "/", no_coin)Read the order book for a HIP-4 outcome:

python

# BTC daily YES = coin "#10" (outcome 1, side 0 → encoding = 10*1+0 = 10)

book = requests.post(ENDPOINT, json={"type": "l2Book", "coin": "#10"}).json()

bids = book["levels"][0]

asks = book["levels"][1]

print(f"Best bid: {bids[0]['px']} Best ask: {asks[0]['px']}")Note: The standard

hyperliquid-python-sdkdoesn’t know about HIP-4 out of the box — itscoin_to_assetmap is built fromspotMetaonly and won’t resolve#10. You need to fetchoutcomeMeta, compute asset IDs (100_000_000 + 10 * outcome_id + side), and inject them into the SDK’s resolver. The Chainstack HIP-4 trading guide has the full SDK patch and working order placement code.

Chainstack’s Hyperliquid nodes support both HTTP REST polling and WebSocket streaming — critical for settlement-burst handling when a daily BTC binary resolves and thousands of positions settle simultaneously.

Want a working starting point? The chainstacklabs/hyperliquid-hip-4 repo on GitHub includes learning examples and a passive market-maker bot for HIP-4 outcome markets — clone it, drop in your Chainstack endpoint, and you have a baseline to build from.

The Chainstack performance dashboard tracks real-time Hyperliquid latency across EU, JP, and US West regions — use it to select the optimal region before deploying your strategy. Hyperliquid is one of eight chains currently tracked (alongside Ethereum, Arbitrum, Base, BNB, Monad, Solana, and TON).

Need testnet HYPE for strategy development? Grab from the Chainstack Hyperliquid testnet faucet.

The Hyperliquid tooling documentation on Chainstack Docs covers SDK setup, order signing, and outcome market data access patterns.

Hyperliquid on Chainstack: SOC 2 Type II and ISO 27001 certified, 99.99%+ uptime SLA, Dedicated Nodes with Bolt fast-sync on Dedicated Nodes for rapid archive access, and the Unlimited Node add-on for flat-rate RPS billing — no surprise overage charges when your bot spikes during settlement events.

Infrastructure requirements for production HIP-4 bots

Prediction markets look like simple YES/NO bets. Underneath, they are order-matching systems with the same latency and data-access requirements as any CLOB exchange — and in some ways harder, because settlement events create concentrated bursts of state changes that can overwhelm unprepared infrastructure.

For HIP-4 specifically, three infrastructure concerns separate a production setup from a toy integration:

- Settlement-burst handling — when a binary outcome resolves, every position in that market settles simultaneously. A spike of thousands of order state changes hits the RPC layer in a narrow window. Endpoints without adequate throughput will queue or drop requests exactly when you need them most.

- WebSocket streaming vs. polling — for outcome book depth, real-time fills, and oracle price feeds, WebSocket subscription is the only latency-viable approach. HTTP polling introduces artificial lag at exactly the moments — settlement, high volatility — when you need the freshest data.

- Archive access for strategy backtesting — HIP-4 market history (fills, order cancels, settlement prices) is available via the info endpoint but requires archive-depth access for historical periods beyond the default lookback. Backtesting a recurring BTC binary strategy across 90 days of daily markets requires archive node access.

- Rate limits and burst capacity — Hyperliquid’s public endpoint caps at 100 requests/minute. Production market-making bots, arbitrage strategies between HIP-4 and Polymarket, and vault contracts polling outcome state will blow through this within seconds.

- Cross-product data correlation — HIP-4’s value proposition is margin composability with perps and spot. Any system exploiting this — a delta-neutral vault, a perp hedge with a binary overlay — needs simultaneous low-latency reads from both the perp book and the outcome book on the same connection.

For Polymarket, the equivalent concerns are around Polygon throughput (CTF token splits and merges are on-chain), CLOB V2 API authentication (two-tier EIP-712 + HMAC), WebSocket subscription reliability for real-time fills, and position indexing via the Gamma API for multi-market portfolio management.

Conclusion

The single most important decision criterion for prediction market infrastructure in 2026 is whether you are trading within crypto or about the world. HIP-4 is the better platform for the former; Polymarket dominates the latter — and that division reflects something deeper than feature lists.

- For delta-neutral crypto hedging and perp overlay strategies: HIP-4 — the unified margin account is structurally unavailable on any standalone prediction market platform

- For arbitrage between HIP-4 and Polymarket: HIP-4 as the low-fee leg; Polymarket as the high-fee leg — the structural edge is durable through Phase 1

- For political, sports, geopolitics, and macro qualitative events: Polymarket — UMA resolution, NegRisk multi-outcome, and market depth are not replicated by anything in Phase 1

- For retail users without crypto wallets: Polymarket — fiat onramps, social login, no gas required

- For builders deploying vault contracts or structured products: HIP-4 on HyperEVM — outcome state is readable by smart contracts in a way Polymarket’s CTF tokens simply do not enable

- Watch Phase 2: When Hyperliquid opens permissionless builder deployment with external oracle integrations, the political and sports market gap begins to close. The 1M HYPE stake bar is high; the teams willing to meet it will be well-capitalized and motivated.

FAQ

HIP-4 outcome contracts are settled in USDH and live on the same matching engine as Hyperliquid perps and spot, meaning they share unified portfolio margin with other positions. A regular prediction market (Polymarket, Kalshi) is a standalone platform where your capital is isolated — you cannot offset a prediction market position against a derivatives position in the same margin account.

Yes, but they are separate platforms with separate collateral. HIP-4 requires USDH on Hyperliquid; Polymarket requires pUSD on Polygon. Arbitrage between the two is technically feasible but requires infrastructure on both chains and collateral management across two ecosystems. Most traders start on one platform and extend to the other as a specific strategy justifies it.

No — winning Polymarket shares always redeem for exactly $1.00 with no fee deducted from the payout. Fees on Polymarket appear as the bid-ask spread in the CLOB and, on certain market categories under CLOB V2 (particularly 15-minute crypto markets), as explicit taker fees that peak around 1.56–1.80% at 50% probability.

At minimum: a WebSocket connection to the HIP-4 outcome book (not just HTTP polling), archive node access for historical market data, and throughput above the 100 req/min public endpoint cap. A Chainstack Dedicated Node removes the rate limit ceiling and provides WebSocket streaming. For settlement-burst handling — when all positions in a daily BTC binary resolve simultaneously — dedicated infrastructure is not optional.

No. Hyperliquid geo-blocks US users on both the trading interface and API. Polymarket’s international exchange also blocks US users, but Polymarket has a CFTC-licensed US-facing product via the QCEX acquisition (July 2025) and is actively pursuing CFTC approval to re-open the main exchange to US traders as of April 2026.

Builders stake 1,000,000 HYPE per deployment slot — slashable if validators determine the builder manipulated an oracle, caused invalid state transitions, or experienced prolonged downtime. One slot recycles across many sequential markets in a series, so a builder deploying a daily BTC binary that runs for 365 days only needs one slot staked for the entire year. Slashed tokens are burned, not redistributed to stakers.

More guides on the Chainstack blog

Building a HIP-4 or Polymarket strategy is one piece of a larger stack. If you want to go deeper on either platform’s infrastructure, these posts cover the terrain:

Hyperliquid

- Hyperliquid HIPs explained: HIP-1 to HIP-4 — the full governance arc from token standard to outcome contracts, with step-function settlement mechanics and builder economy details

- What is Hyperliquid? RPC, API, and trading infrastructure — HyperCore vs HyperEVM architecture, API surfaces, and how developers plug in

- How to build a Hyperliquid trading bot — from RPC node selection to a working grid bot with WebSocket feeds and order execution

- Hyperliquid architecture: Clearinghouse, Agent Keys, cross-margin — the unified state tree that makes cross-margin between perps and spot (and now outcomes) possible

Polymarket

- Integrating Chainstack with OpenClaw bot for Polymarket — LLM-powered arbitrage across Polymarket markets via messenger interface

- How to build a Polymarket bot using Polygon RPC — correlated market detection, hedge portfolios, and why reliable Polygon RPC matters for prediction market bots